The Impact of Credit Score on Auto Insurance Rates Explained

Explore the impact of credit score on auto insurance rates explained. Understand how your credit history can affect your car insurance premiums.

Explore the impact of credit score on auto insurance rates explained. Understand how your credit history can affect your car insurance premiums.

The Impact of Credit Score on Auto Insurance Rates Explained

Understanding Credit Scores and Auto Insurance Premiums

Ever wondered why your credit score, something usually associated with loans and mortgages, pops up when you're trying to get a car insurance quote? You're not alone. Many people are surprised to learn that their credit history can significantly influence how much they pay for auto insurance. In fact, in most U.S. states and some other regions, insurance companies use what's called a 'credit-based insurance score' as one of the key factors in determining your premium. This isn't your FICO score, but a specialized score derived from your credit report, designed to predict the likelihood of you filing a claim.

The logic behind this practice, according to insurers, is that there's a statistical correlation between a person's credit history and their likelihood of filing an insurance claim. Studies have shown that individuals with lower credit-based insurance scores tend to file more claims and more expensive claims than those with higher scores. While this might seem unfair or unrelated at first glance, insurers view it as a reliable predictor of risk. A higher credit-based insurance score often translates to lower premiums, as you're perceived as a lower risk to insure. Conversely, a lower score can lead to higher rates.

It's important to note that not all states allow the use of credit scores in setting auto insurance rates. California, Hawaii, and Massachusetts are notable exceptions where this practice is prohibited. However, in the vast majority of the U.S., it's a standard part of the underwriting process. For consumers, understanding this connection is crucial for managing their insurance costs and making informed decisions.

How Credit Based Insurance Scores Are Calculated Key Factors

So, what exactly goes into a credit-based insurance score? It's not just about having a lot of debt or a few late payments. Insurers look at several aspects of your credit report to generate this specialized score. While the exact algorithms are proprietary to each insurance company and credit bureau, here are the key factors that generally influence your credit-based insurance score:

- Payment History: This is arguably the most important factor. Consistently paying your bills on time demonstrates financial responsibility. Late payments, collections, bankruptcies, or foreclosures can significantly lower your score.

- Amounts Owed: How much debt you have relative to your credit limits (your credit utilization ratio) plays a role. High credit utilization can indicate financial strain, which insurers might interpret as a higher risk.

- Length of Credit History: A longer history of responsible credit use generally leads to a better score. It gives insurers more data to assess your financial habits over time.

- New Credit: Opening many new credit accounts in a short period can be seen as a risk factor, as it might suggest financial instability or an increased likelihood of taking on more debt.

- Credit Mix: Having a healthy mix of different types of credit (e.g., credit cards, installment loans, mortgages) can positively impact your score, showing you can manage various forms of credit responsibly.

It's crucial to remember that these scores are not identical to the FICO or VantageScore scores used for lending. They are specifically tailored for insurance purposes, but they draw from the same underlying data in your credit report. Therefore, improving your general credit health will almost certainly lead to a better credit-based insurance score.

The Direct Impact of Credit Score on Auto Insurance Premiums Real World Examples

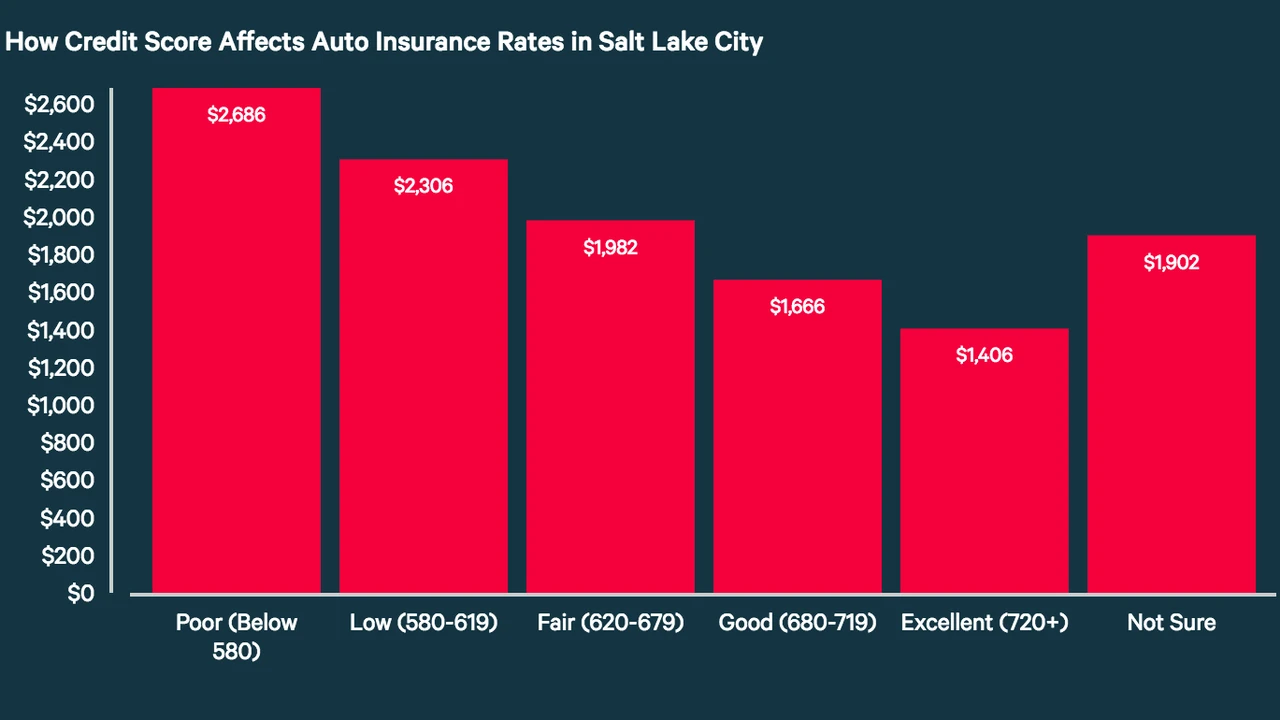

Let's get down to brass tacks: how much can your credit score actually affect your auto insurance premiums? The impact can be substantial. While the exact figures vary widely based on your location, age, driving record, vehicle type, and the specific insurer, studies and industry data consistently show that drivers with excellent credit pay significantly less than those with poor credit.

For instance, a driver with excellent credit (typically a credit-based insurance score in the top tier) might pay 20% to 50% less for the same coverage compared to a driver with poor credit (in the lowest tier). Some reports even suggest differences of over 100% in certain scenarios. This means if a driver with excellent credit pays $1,000 per year for auto insurance, a driver with poor credit could be paying $1,500, $2,000, or even more for the exact same policy from the same company.

Consider these hypothetical scenarios:

- Scenario 1: The Responsible Driver

Sarah, 35, lives in Texas, drives a 2020 Honda Civic, has a clean driving record, and an excellent credit score (e.g., 800+ FICO equivalent). She might receive quotes around $1,200 per year for full coverage. - Scenario 2: The Financially Stressed Driver

Mark, 35, also lives in Texas, drives the same 2020 Honda Civic, has a clean driving record, but a poor credit score (e.g., below 580 FICO equivalent) due to some past financial difficulties. His quotes for the exact same full coverage might be closer to $2,000 - $2,500 per year. - Scenario 3: The Improving Driver

Maria, 40, had a rough patch financially a few years ago, resulting in a fair credit score (e.g., 580-669 FICO equivalent). She's been diligently improving her credit. Her initial quotes were around $1,800. After a year of consistent on-time payments and reducing debt, her credit score improved, and her renewal quote dropped to $1,500.

These examples highlight that your credit score isn't just a minor factor; it's a major determinant of your auto insurance costs. Improving it can lead to substantial savings over time.

Strategies to Improve Your Credit Score for Lower Auto Insurance Rates

The good news is that your credit score isn't set in stone. You can take proactive steps to improve it, which in turn can lead to lower auto insurance premiums. Here are some effective strategies:

Pay Your Bills On Time Every Time The Foundation of Good Credit

This is the single most impactful action you can take. Payment history accounts for a significant portion of your credit score. Set up automatic payments, calendar reminders, or use budgeting apps to ensure you never miss a due date. Even a single late payment can ding your score, and multiple late payments can have a severe, long-lasting negative effect.

Reduce Your Credit Utilization Ratio Manage Debt Wisely

Your credit utilization ratio is the amount of credit you're using compared to your total available credit. Aim to keep this ratio below 30%. For example, if you have a credit card with a $10,000 limit, try to keep your balance below $3,000. Paying down credit card balances is an excellent way to quickly improve this ratio and, consequently, your score. If you have multiple cards, focus on paying down the ones with the highest balances first.

Avoid Opening Too Many New Credit Accounts Strategically Apply

While it might seem counterintuitive, opening several new credit accounts in a short period can temporarily lower your score. Each application results in a 'hard inquiry' on your credit report, which can slightly reduce your score. Only apply for new credit when you genuinely need it and are confident you'll be approved. Space out your applications if possible.

Check Your Credit Report Regularly Spot Errors and Fraud

You're entitled to a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once every 12 months via AnnualCreditReport.com. Review these reports carefully for any inaccuracies or fraudulent activity. Errors, such as incorrect late payments or accounts you didn't open, can negatively impact your score. If you find an error, dispute it immediately with the credit bureau and the creditor. Correcting errors can sometimes lead to a quick boost in your score.

Maintain a Long Credit History Don't Close Old Accounts

The length of your credit history contributes to your score. Older accounts, especially those with a good payment history, demonstrate a long track record of responsible borrowing. Even if you don't use an old credit card much, it's often better to keep it open (as long as it doesn't have an annual fee) to maintain your average age of accounts and your overall available credit.

Diversify Your Credit Mix Show Responsible Management

Having a mix of different types of credit, such as installment loans (like a car loan or mortgage) and revolving credit (like credit cards), can positively impact your score. It shows you can manage various financial obligations responsibly. However, don't take on debt you don't need just to diversify your credit mix.

Specific Products and Services to Help Manage Your Credit

Improving your credit score can feel like a daunting task, but there are many tools and services available to help you monitor your progress and stay on track. While these don't directly improve your score, they provide the information and guidance you need to make smart financial decisions.

Credit Monitoring Services Stay Informed

These services track changes to your credit report and alert you to suspicious activity, potential fraud, or significant score changes. Many also provide your credit score and detailed insights into what's affecting it.

- Experian Boost: This free service from Experian allows you to potentially increase your FICO score by including on-time utility and telecom payments that aren't typically part of your credit report. It's a unique way to add positive payment history.

- Credit Karma: Offers free credit scores (VantageScore 3.0 from TransUnion and Equifax), credit reports, and monitoring. It provides personalized recommendations for improving your score and finding better financial products.

- MyFICO: While some features are paid, MyFICO offers access to your FICO scores (the most widely used scores by lenders) and reports from all three bureaus. It provides detailed explanations of what's impacting your score.

- Identity Guard: Focuses heavily on identity theft protection but also includes credit monitoring and alerts, providing peace of mind while you work on your credit.

Secured Credit Cards Build Credit Safely

If you have poor credit or no credit history, a secured credit card can be an excellent tool. You put down a deposit, which becomes your credit limit, and then use the card like a regular credit card. Your payments are reported to credit bureaus, helping you build a positive payment history.

- Discover it Secured Credit Card: A popular choice, it offers cash back rewards and reports to all three major credit bureaus. After responsible use, Discover may transition you to an unsecured card.

- Capital One Platinum Secured Credit Card: Another solid option, it often requires a lower security deposit than your credit limit, making it more accessible for some.

Credit Builder Loans A Structured Approach

These loans are designed specifically to help people build credit. Instead of receiving the money upfront, the loan amount is held in a savings account while you make regular payments. Once the loan is paid off, you receive the money, and your payment history is reported to credit bureaus.

- Self Credit Builder Account: This service offers credit builder loans that report to all three major credit bureaus. They also offer a secured credit card option once you've made a few payments.

- Local Credit Unions: Many local credit unions offer their own versions of credit builder loans, often with competitive rates and personalized service.

Budgeting and Debt Management Tools Take Control

Effective budgeting and debt management are fundamental to improving your credit score. These tools help you track spending, create budgets, and develop strategies to pay down debt.

- You Need A Budget (YNAB): A popular budgeting app that helps you assign every dollar a job, promoting mindful spending and debt reduction. (Subscription based, around $14.99/month or $99/year).

- Mint: A free budgeting app that links to your bank accounts and credit cards, allowing you to track spending, create budgets, and monitor your financial health.

- National Foundation for Credit Counseling (NFCC): A non-profit organization that offers free or low-cost credit counseling, debt management plans, and educational resources.

Remember, consistency is key. It takes time to build or rebuild credit, but the effort will pay off not only in lower auto insurance rates but also in better access to loans, mortgages, and other financial products.

When to Shop for Auto Insurance Based on Credit Score Changes

Your credit score isn't static; it changes over time as you manage your finances. This means your auto insurance rates aren't static either. If you've been diligently working on improving your credit, it's wise to periodically shop around for new auto insurance quotes.

Annual Review and Quote Comparison

Even if your credit hasn't changed dramatically, it's a good practice to compare quotes from multiple insurers at least once a year, typically around your policy renewal time. This ensures you're always getting the best possible rate. If your credit score has improved significantly, this annual review becomes even more critical.

Significant Credit Score Improvement

If you've seen a substantial jump in your credit score (e.g., moving from 'poor' to 'fair' or 'fair' to 'good'), don't wait for your renewal. Get new quotes immediately. Insurers will pull your credit-based insurance score when you apply for a new policy, and a better score could unlock significant savings right away. You might even consider switching mid-policy if the savings are substantial enough to offset any cancellation fees.

Life Events Affecting Credit

Certain life events can impact your credit score, both positively and negatively. For example, paying off a large loan (like a student loan or car loan) can improve your credit utilization and overall score. Conversely, a major financial setback could lower it. After any significant financial event that might have altered your credit standing, it's a good idea to check your credit score and then re-evaluate your insurance options.

Don't Forget Other Factors

While credit score is a major factor, remember that insurers also consider your driving record, vehicle type, age, location, and claims history. Even with an excellent credit score, a recent accident or moving violation can still lead to higher premiums. Always strive for safe driving habits in addition to good financial management.

The Debate and Future of Credit Based Insurance Scoring

The use of credit-based insurance scores is not without controversy. Critics argue that it unfairly penalizes low-income individuals or those who have experienced financial hardship, creating a cycle where they pay more for essential services like insurance, even if they are safe drivers. They contend that it's discriminatory and not a direct measure of driving risk.

Consumer advocacy groups often push for legislation to ban or limit the use of credit scores in insurance underwriting, citing concerns about fairness and accessibility. As mentioned earlier, some states have already taken this step, and others continue to debate the issue.

On the other hand, insurance companies defend the practice by stating that it's a statistically valid predictor of risk and allows them to price policies more accurately, ultimately benefiting all policyholders by preventing higher rates across the board. They argue that removing this factor would force them to rely more heavily on other, potentially less precise, risk indicators.

The future of credit-based insurance scoring is uncertain. With increasing scrutiny and advancements in telematics (usage-based insurance that tracks actual driving behavior), there might be a shift towards more direct measures of driving risk. However, for now, in most places, your credit score remains a powerful determinant of your auto insurance premiums. Understanding this relationship and actively managing your credit health is one of the most effective ways to secure more affordable car insurance rates.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)