3 Best Strategies for Affordable Car Insurance in Malaysia

Learn 3 best strategies for affordable car insurance in Malaysia. Find competitive rates and essential coverage for your vehicle in Malaysia.

Learn 3 best strategies for affordable car insurance in Malaysia. Find competitive rates and essential coverage for your vehicle in Malaysia.

3 Best Strategies for Affordable Car Insurance in Malaysia

Hey there, fellow Malaysian drivers! Let's talk about something super important but often a bit confusing: car insurance. We all need it, it's mandatory, but nobody wants to pay an arm and a leg for it, right? Especially with the rising cost of living, every Ringgit saved counts. So, if you're looking to slash your car insurance premiums without compromising on essential coverage, you've come to the right place. We're going to dive deep into three of the best strategies to help you find competitive rates and ensure your vehicle is well-protected on Malaysia's bustling roads.

Forget about just renewing with the same old provider year after year without a second thought. That's often the most expensive way to do things! Instead, let's get smart about it. We'll cover everything from understanding your policy to leveraging technology and making informed choices. Ready to save some money? Let's roll!

Strategy 1 Compare and Shop Around for Malaysian Car Insurance

This might sound like a no-brainer, but you'd be surprised how many people skip this crucial step. Sticking with your current insurer out of habit or convenience is a common pitfall that can cost you hundreds, if not thousands, of Ringgit annually. The Malaysian car insurance market is competitive, with many players vying for your business. Each insurer has its own underwriting criteria, risk assessment models, and promotional offers, which means prices can vary significantly for the exact same coverage.

Why Comparing is Key for Affordable Car Insurance Malaysia

- Different Pricing Models: Insurers use various factors like your age, driving experience, vehicle model, location, and even occupation to calculate premiums. What one insurer considers high-risk, another might view as moderate, leading to different quotes.

- Promotional Offers and Discounts: Companies frequently run campaigns, especially during festive seasons or year-end. These can include discounts for online purchases, new customers, or specific payment methods. You won't know about them if you don't look!

- No-Claim Discount NCD Impact: While your NCD is transferable, how different insurers apply it or what base premium they start with can still lead to varying final prices.

- Policy Features and Add-ons: Beyond the basic coverage, different insurers offer unique add-ons or benefits. Comparing helps you find a policy that perfectly matches your needs without paying for extras you don't want.

How to Effectively Compare Car Insurance in Malaysia

Gone are the days of calling multiple agents or visiting various branches. The internet has made comparing car insurance in Malaysia incredibly easy and efficient. Here's how you can do it:

Online Comparison Platforms for Malaysian Auto Insurance

These platforms are your best friends for quick comparisons. They allow you to input your details once and get quotes from multiple insurers simultaneously. It's a huge time-saver and often highlights the cheapest options right away.

- Bjak: Arguably the most popular and comprehensive platform in Malaysia. Bjak allows you to compare quotes from over 10 leading insurers, including Allianz, Etiqa, Takaful Malaysia, Zurich, and more. They often have exclusive discounts and make the renewal process super smooth. You can get quotes for both conventional and Takaful insurance.

- PolicyStreet: Another strong contender, PolicyStreet offers comparisons from a good range of insurers and also provides personalized advice. They focus on making insurance easy to understand and accessible.

- iBanding: While perhaps not as widely known for direct comparison as Bjak, iBanding provides valuable insights into insurer performance and customer satisfaction, which can indirectly help you choose. They also offer comparison services.

Direct Insurer Websites for Car Insurance Quotes Malaysia

While comparison sites are great, it's also a good idea to check a few direct insurer websites, especially if you have a preferred company or if a comparison site doesn't include all insurers. Sometimes, insurers offer exclusive online discounts directly on their own platforms.

- Etiqa: Known for its user-friendly online platform and often competitive pricing, especially for comprehensive policies. They frequently offer online discounts and instant policy issuance.

- Allianz: A major player with a strong reputation. Their website allows for easy quote generation and policy management.

- Zurich: Offers a good range of products and often has competitive rates, particularly for certain vehicle types or demographics.

- Takaful Malaysia: If you're looking for Shariah-compliant insurance, Takaful Malaysia is a leading provider. Their online platform is efficient for getting quotes and renewing.

Tips for Comparing Effectively

- Be Accurate: Ensure all information you provide (vehicle details, NCD, driver history) is accurate. Inaccurate info can lead to invalid quotes or issues during claims.

- Compare Apples to Apples: Make sure you're comparing policies with similar coverage types (e.g., comprehensive vs. third-party), sum insured, and add-ons.

- Read the Fine Print: Don't just look at the price. Understand the policy wording, exclusions, and terms and conditions.

- Check for Hidden Fees: Some platforms or insurers might have administrative fees. Clarify these upfront.

Strategy 2 Optimize Your Policy and Vehicle for Lower Premiums in Malaysia

Once you've done your comparison homework, the next step is to look inward. How can you make yourself or your vehicle more attractive to insurers? There are several factors within your control that can significantly impact your premium. This strategy is all about being a smart consumer and understanding how insurers assess risk.

Leveraging No-Claim Discount NCD for Cheaper Car Insurance Malaysia

Your NCD is your golden ticket to cheaper insurance. It's a discount offered for not making any claims during your policy period. In Malaysia, the NCD structure is standardized:

- 1 year without claim: 25% NCD

- 2 years without claim: 30% NCD

- 3 years without claim: 38.33% NCD

- 4 years without claim: 45% NCD

- 5 years or more without claim: 55% NCD

This 55% NCD is the maximum you can get, and it's a massive saving! Always protect your NCD. If you have a minor accident, sometimes it's cheaper to pay for the repairs out of pocket rather than making a claim and losing your NCD. Do the math!

NCD Protector Add-on for Malaysian Auto Insurance

Some insurers offer an NCD Protector add-on. For a small additional premium, this add-on protects your NCD even if you make one claim during the policy year. It's worth considering, especially if your NCD is high (e.g., 55%) and you want peace of mind.

Choosing the Right Coverage Type for Your Car in Malaysia

Not every car needs a full comprehensive policy. Understanding the different types of coverage can help you save money, especially for older vehicles.

- Comprehensive Policy: This is the most extensive coverage, protecting against damage to your own car (due to accident, fire, theft), third-party damage, and bodily injury. It's highly recommended for newer or more valuable cars.

- Third-Party Fire and Theft (TPFT): Covers third-party damage/injury, and also covers your car if it's stolen or catches fire. It's a good middle-ground for slightly older cars where comprehensive might be too expensive, but you still want protection against major losses.

- Third-Party Only (TPO): The most basic and cheapest option. It only covers damage or injury to third parties. This is usually only suitable for very old, low-value cars where the cost of repairing your own vehicle isn't a major concern.

Evaluate your car's market value. If your car is 10+ years old and its market value is low, a TPFT or TPO policy might be more cost-effective than comprehensive, as the premium for comprehensive might be disproportionately high compared to the car's value.

Increasing Your Deductible Excess for Lower Premiums Malaysia

The deductible (or excess) is the amount you agree to pay out of pocket before your insurance kicks in for a claim. A higher deductible generally means a lower premium. This is because you're taking on more of the initial risk yourself.

For example, if your policy has a standard RM500 deductible, and you opt for an RM1,000 deductible, your premium will likely decrease. This strategy works best if you're a careful driver and can comfortably afford to pay the higher deductible in case of an accident. Don't choose a deductible you can't afford!

Considering Add-ons Wisely for Malaysian Car Insurance

Add-ons can significantly increase your premium. While some are essential, others might be optional depending on your needs.

- Windscreen Coverage: Highly recommended in Malaysia due to frequent stone chips. It's usually a separate add-on and making a claim on it typically doesn't affect your NCD.

- Special Perils (Flood, Landslide, etc.): Absolutely crucial if you live in or frequently drive through flood-prone areas. Given Malaysia's weather, this is often a wise investment.

- All Drivers Coverage: If multiple people drive your car, this is important. Otherwise, you might only need coverage for named drivers.

- Waiver of Betterment: For older cars (usually 5 years or older), when parts are replaced after an accident, insurers might apply a 'betterment' clause, meaning you pay a portion of the new part's cost. This add-on waives that. Consider if your car is older.

Review your add-ons annually. Do you still need all of them? Are there new ones that would be beneficial?

Driving Safely and Maintaining a Clean Record for Cheaper Auto Insurance Malaysia

This is perhaps the most straightforward way to save money. A clean driving record (no accidents, no traffic violations) directly translates to a higher NCD and makes you a lower-risk driver in the eyes of insurers. Some insurers even offer discounts for drivers who haven't had any claims for a certain number of years, even beyond the NCD.

Vehicle Modifications and Their Impact on Malaysian Car Insurance

Be cautious with modifications. While some aesthetic or performance upgrades might seem cool, they can increase your premium or even void your policy if not declared. Insurers view modifications as increasing risk (e.g., higher theft risk for expensive rims, higher accident risk for performance mods). Always inform your insurer about any significant modifications.

Strategy 3 Leverage Discounts and Special Programs for Malaysian Auto Insurance Savings

Beyond comparing and optimizing your policy, there are often various discounts and special programs available that can further reduce your premiums. You just need to know where to look and what to ask for!

Common Discounts Offered by Malaysian Car Insurers

Don't be shy to ask your insurer or check their website for these common discounts:

- Online Purchase Discount: Many insurers offer a small discount (e.g., 5-10%) if you purchase or renew your policy directly through their website or app. This saves them administrative costs, and they pass some of those savings to you.

- Loyalty Discount: Some insurers reward long-term customers. If you've been with the same company for several years, inquire if they have a loyalty program.

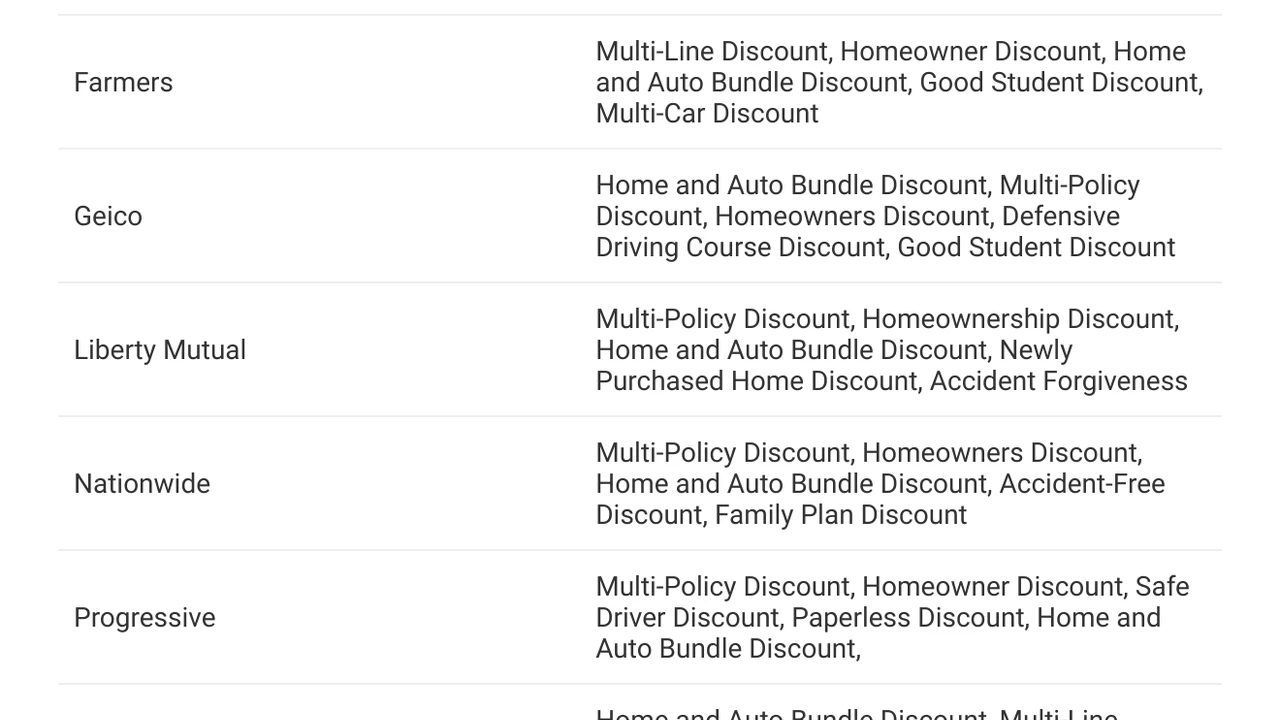

- Multi-Policy Discount: If you have other insurance policies with the same company (e.g., home insurance, life insurance, medical insurance), they might offer a discount for bundling. This is a great way to consolidate and save.

- Good Driver Discount: Beyond NCD, some insurers have specific programs for drivers with a consistently clean record over many years.

- Anti-Theft Device Discount: If your car is equipped with approved anti-theft devices (e.g., alarm systems, immobilizers, GPS trackers), some insurers might offer a discount as it reduces the risk of theft.

- Low Mileage Discount: If you don't drive much (e.g., you work from home, use public transport often), some insurers might offer a discount based on your annual mileage. This is becoming more common with telematics.

- Occupation-Based Discounts: Certain professions (e.g., teachers, civil servants) might qualify for special rates with some insurers. It's always worth asking!

- Payment Method Discounts: Sometimes, paying your premium annually in a lump sum can be cheaper than monthly installments, or using a specific credit card might offer cashback or points that effectively reduce your cost.

Telematics and Usage-Based Insurance UBI in Malaysia

This is a growing trend in Malaysia and a fantastic way for safe drivers to save money. Telematics involves installing a small device in your car or using a smartphone app that monitors your driving habits (speed, braking, acceleration, mileage, time of day you drive). Based on your driving score, you can get discounts on your premiums.

Popular Telematics Programs in Malaysia

- Drive Less Save More by Etiqa: Etiqa offers a program where you can get rebates based on your mileage. The less you drive, the more you save. This is great for those who don't commute daily or have multiple cars.

- Drive Smart by Allianz: Allianz has a telematics program that rewards safe driving. By monitoring your driving behavior, you can earn discounts on your renewal premium.

- AXA FlexiDrive: AXA (now part of Generali) also offers a telematics-based insurance that provides discounts for good driving behavior and lower mileage.

If you're confident in your driving skills and don't mind being monitored, UBI can lead to significant savings. It's a win-win: you drive safer, and you pay less.

Consider Takaful Insurance for Shariah-Compliant Options in Malaysia

For Muslim drivers, or anyone interested in an ethical insurance model, Takaful insurance is a Shariah-compliant alternative to conventional insurance. It operates on principles of mutual assistance and shared responsibility. While the core coverage is similar, the underlying philosophy and how surpluses are managed differ.

Leading Takaful Providers in Malaysia

- Takaful Malaysia: A prominent Takaful provider offering competitive rates and a wide range of motor Takaful products. They are known for their online convenience and often have attractive promotions.

- Etiqa Takaful: Etiqa also has a strong Takaful arm, providing comprehensive and flexible motor Takaful plans.

It's worth getting quotes from Takaful providers as well, as their pricing can sometimes be more competitive depending on your profile.

Review Your Sum Insured for Malaysian Car Insurance

The sum insured is the maximum amount your insurer will pay if your car is a total loss or stolen. This amount is usually based on your car's market value. However, market values depreciate over time. Ensure your sum insured is updated annually to reflect your car's current market value. Insuring your car for more than its worth means you're overpaying on premiums without getting any extra benefit in a total loss scenario. Conversely, under-insuring can leave you short if something happens.

Most insurers use standard market value guides (like ISM or Glass's Guide) to determine this, but you can also get an independent valuation if you feel it's necessary.

Maintain Your Vehicle Regularly for Better Insurance Rates Malaysia

While not a direct discount, a well-maintained vehicle is less prone to breakdowns and accidents caused by mechanical failure. This contributes to a clean driving record and reduces the likelihood of making claims, thereby protecting your NCD and keeping your premiums low in the long run. Some insurers might even offer minor incentives for vehicles that undergo regular servicing at authorized centers, though this is less common as a direct discount.

Putting It All Together Your Action Plan for Affordable Car Insurance in Malaysia

So, you've got the strategies, now let's talk about how to implement them. Think of your car insurance renewal as an annual financial review. It's not just a chore; it's an opportunity to save money!

Step-by-Step Guide to Securing Cheaper Car Insurance in Malaysia

- Start Early: Don't wait until the last minute. Begin comparing quotes at least 2-3 weeks before your policy expires. This gives you ample time to research, compare, and make an informed decision without feeling rushed.

- Gather Your Documents: Have your existing policy details, NCD statement, vehicle registration card (or e-Geran details), and driver's license handy. This will speed up the quote process.

- Use Online Comparison Platforms: Head over to Bjak or PolicyStreet. Input your details accurately and get quotes from multiple insurers. Pay attention to the coverage details, not just the price.

- Check Direct Insurer Websites: After using comparison sites, visit the websites of 2-3 top contenders directly. Sometimes, they offer exclusive online discounts not available elsewhere.

- Review Your Coverage Needs: Is your car older now? Do you still need comprehensive, or would TPFT suffice? Are all your add-ons still necessary? Adjust your coverage to match your current needs and your car's value.

- Consider a Higher Deductible: If you're a safe driver and have an emergency fund, opting for a higher deductible can significantly lower your premium.

- Inquire About Discounts: Don't assume insurers will automatically apply all eligible discounts. Ask about online purchase discounts, multi-policy discounts, anti-theft device discounts, and any occupation-based offers.

- Explore Telematics: If you're a low-mileage or safe driver, ask about telematics programs like Etiqa's Drive Less Save More or Allianz's Drive Smart.

- Read the Policy Wording: Before finalizing, always read the policy document carefully. Understand what's covered, what's excluded, and the terms and conditions.

- Make the Purchase: Once you're satisfied, proceed with the purchase. Most online platforms and direct insurer websites allow for instant policy issuance and e-delivery of documents.

A Quick Look at Some Popular Malaysian Car Insurance Products and Their Features

While specific pricing depends on your individual profile, here's a general overview of some popular products and what they typically offer, helping you understand what to look for:

1. Etiqa Comprehensive Private Car Insurance

- Key Features: Often praised for its user-friendly online platform and competitive pricing. Includes standard comprehensive coverage (own damage, third-party liability, fire, theft).

- Unique Selling Points: Often offers free personal accident coverage for the driver and passengers, 24/7 roadside assistance, and a 'Drive Less Save More' telematics option for mileage-based rebates. They also have a strong Takaful arm.

- Target User: Drivers looking for a balance of comprehensive coverage, good customer service, and potential savings through telematics or online discounts.

- Typical Price Range: Varies widely, but often among the more affordable options for comprehensive policies, especially with online discounts.

2. Allianz Motor Comprehensive Insurance

- Key Features: A well-established insurer with a strong reputation. Offers robust comprehensive coverage, including third-party property damage, bodily injury, own damage, fire, and theft.

- Unique Selling Points: Known for efficient claims processing and a wide network of panel workshops. Offers add-ons like 'Allianz Road Rangers' for enhanced roadside assistance and 'Drive Smart' telematics for safe driver discounts.

- Target User: Drivers who prioritize a reputable insurer, comprehensive support services, and potentially benefit from telematics.

- Typical Price Range: Generally competitive, but can be slightly higher than some budget options, reflecting their service and network.

3. Takaful Malaysia Motor Takaful

- Key Features: Shariah-compliant alternative to conventional insurance. Offers similar comprehensive coverage but operates on principles of mutual assistance and shared responsibility.

- Unique Selling Points: Often provides a 'Cashback' or 'Surplus Sharing' feature, where participants may receive a portion of any underwriting surplus if no claims are made. Strong online presence and competitive pricing.

- Target User: Muslim drivers seeking Shariah-compliant insurance, or anyone interested in an ethical insurance model with potential cashback benefits.

- Typical Price Range: Often very competitive, especially when considering the potential for surplus sharing.

4. Zurich Z-Driver Comprehensive Motor Insurance

- Key Features: Offers comprehensive coverage with various customizable add-ons. Focuses on flexibility to tailor the policy to individual needs.

- Unique Selling Points: Provides options for waiver of betterment, windscreen coverage, special perils, and personal accident coverage. Known for good customer support.

- Target User: Drivers who want a customizable policy with a good range of add-ons and reliable service.

- Typical Price Range: Generally competitive, with pricing varying based on the chosen add-ons and vehicle profile.

Remember, these are just examples. The best product for you will depend on your specific vehicle, driving history, location, and desired level of coverage. Always get multiple quotes and compare the features side-by-side.

By actively engaging with these strategies – comparing diligently, optimizing your policy, and leveraging available discounts – you're not just renewing your car insurance; you're taking control of your finances and ensuring you get the best possible deal in the Malaysian market. Happy driving, and even happier saving!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)