Comparing Auto Insurance for Electric Vehicles in the USA

Explore comparing auto insurance for electric vehicles in the USA. Understand unique coverage needs and potential discounts for EVs.

Explore comparing auto insurance for electric vehicles in the USA. Understand unique coverage needs and potential discounts for EVs.

Comparing Auto Insurance for Electric Vehicles in the USA

The Rise of Electric Vehicles and Auto Insurance Implications

Hey there, future-forward drivers! So, you're thinking about going electric, or maybe you've already made the switch to an EV. That's awesome! Electric vehicles (EVs) are no longer just a niche market; they're becoming a significant part of the automotive landscape in the USA. From sleek Teslas to practical Nissan Leafs and the ever-growing range of electric trucks and SUVs, EVs offer a ton of benefits: they're quieter, often quicker, and definitely better for the environment. But here's a question that often pops up: how does auto insurance for these high-tech beauties compare to their gasoline-powered counterparts?

It's a valid concern, and one that many EV owners or prospective buyers ponder. The truth is, insuring an electric vehicle isn't exactly the same as insuring a traditional car. There are unique factors at play that can influence your premiums, coverage needs, and even the claims process. We're talking about advanced battery technology, specialized repair requirements, and sometimes, a higher initial purchase price. All these elements can shift the insurance landscape a bit.

In this comprehensive guide, we're going to dive deep into the world of EV auto insurance in the USA. We'll break down what makes EV insurance different, explore the unique coverage options you might need, and, most importantly, help you understand how to find the best deals and potential discounts. We'll even look at some specific EV models and how their insurance costs might vary. So, buckle up, because we're about to electrify your understanding of auto insurance!

Unique Coverage Needs for Electric Vehicles EV Insurance Essentials

Alright, let's get down to brass tacks. What exactly makes insuring an EV different? It largely boils down to a few key areas:

Battery Coverage and Replacement Costs

The battery is the heart of your EV, and it's often the most expensive component. If your EV's battery is damaged in an accident, or even due to a manufacturing defect (though that's usually covered by the manufacturer's warranty), replacing it can cost a pretty penny – sometimes tens of thousands of dollars. This high replacement cost can directly impact your insurance premiums. Some insurers might offer specific battery coverage or include it within comprehensive coverage, but it's crucial to confirm the extent of this protection. You want to make sure you're not left with a massive bill if something happens to your power source.

Charging Equipment Protection Home and Public Chargers

Another unique aspect of EV ownership is the charging infrastructure. Whether you have a Level 2 charger installed at home or rely on public charging stations, this equipment is vital. What happens if your home charger is damaged by a power surge or stolen? Or if a public charging station causes damage to your vehicle's charging port? Some standard auto insurance policies might not explicitly cover this. You might need to look for policies that offer specific coverage for charging equipment, or ensure your homeowner's insurance covers your home charging station. It's a detail often overlooked but super important for EV owners.

Specialized Repair and Maintenance EV Repair Networks

EVs are complex machines, and their repair often requires specialized tools, training, and parts. Not every mechanic shop is equipped to handle EV repairs, especially for advanced components like the electric motor or battery management system. This can lead to higher labor costs and potentially longer repair times, which in turn can influence insurance claims and premiums. Some insurers are starting to partner with certified EV repair networks, which can be a huge plus. When choosing an insurer, it's worth asking about their preferred repair shops for EVs and if they have a network of certified technicians.

Higher Initial Purchase Price and Depreciation

Generally speaking, many EVs still have a higher upfront purchase price compared to similar gasoline-powered cars. A higher vehicle value usually translates to higher insurance premiums because the cost to replace or repair the vehicle is greater. While EV prices are coming down, and government incentives can help, it's still a factor. Also, consider depreciation. While some EVs hold their value well, others might depreciate differently than ICE (internal combustion engine) vehicles. Gap insurance, which covers the difference between what you owe on your car and its actual cash value if it's totaled, can be particularly useful for new EVs.

Factors Influencing EV Auto Insurance Premiums Cost Drivers

So, what exactly drives those insurance premiums for your electric ride? It's a mix of factors, some common to all vehicles, and some specific to EVs:

Vehicle Make Model and Trim EV Specifics

Just like with traditional cars, the specific make, model, and trim of your EV play a huge role. A high-performance Tesla Model S Plaid will likely cost more to insure than a more modest Nissan Leaf. Why? Higher performance often means higher repair costs for specialized parts, and more powerful vehicles can sometimes be associated with a higher risk of accidents (though this isn't always the case for EVs, which often have advanced safety features). Luxury EVs also tend to have more expensive parts and labor for repairs.

Advanced Technology and Safety Features ADAS Impact

EVs are often packed with advanced driver-assistance systems (ADAS) like automatic emergency braking, lane-keeping assist, adaptive cruise control, and sophisticated sensor arrays. While these features are designed to prevent accidents and enhance safety, they can also be incredibly expensive to repair or recalibrate after even a minor fender bender. A damaged sensor in the bumper of an EV could cost significantly more to fix than a simple bumper replacement on an older car. However, some insurers might offer discounts for vehicles equipped with certain ADAS features, as they can reduce the likelihood of certain types of accidents. It's a bit of a double-edged sword.

Driver Profile and Driving Habits Telematics and Usage Based Insurance

Your personal driving record, age, location, and even credit score (in many states) will always be major factors. But for EVs, telematics and usage-based insurance (UBI) programs can be particularly relevant. Many EVs come with built-in connectivity that can track driving habits like mileage, speed, braking, and acceleration. Insurers like Progressive (Snapshot), State Farm (Drive Safe & Save), and Allstate (Drivewise) offer UBI programs that can reward safe EV drivers with lower premiums. If you're a careful driver, this could be a fantastic way to save money.

Location and Charging Infrastructure Regional Differences

Where you live matters. Urban areas with higher traffic density and theft rates typically have higher premiums. But for EVs, the availability of charging infrastructure can also subtly influence rates. In areas with more robust charging networks, insurers might perceive less risk of a driver running out of charge in an unsafe location. Also, the cost of electricity varies by region, which, while not directly impacting premiums, is part of the overall cost of EV ownership.

Potential Discounts for Electric Vehicles EV Savings

Here's the good news! While some aspects of EV insurance can be pricier, there are also specific discounts you might qualify for that can help offset those costs:

Eco Friendly or Green Vehicle Discounts

Many insurance companies are keen to support environmentally friendly choices. Some insurers offer specific 'green vehicle' or 'eco-friendly' discounts for owning an EV or hybrid. These can vary, so it's always worth asking your provider if they have such a program. Companies like Farmers and Travelers have been known to offer these types of discounts.

Advanced Safety Feature Discounts ADAS Incentives

As mentioned earlier, while ADAS can increase repair costs, their primary purpose is accident prevention. Insurers often provide discounts for vehicles equipped with features like automatic emergency braking, lane departure warning, blind-spot monitoring, and adaptive headlights. Since many EVs come standard with these technologies, you're likely to qualify for several of these safety discounts.

Low Mileage Discounts for EVs

If you primarily use your EV for short commutes or have access to public transport, you might drive fewer miles than the average driver. Many insurers offer low mileage discounts, which can be particularly beneficial for EV owners who might not use their electric car for long road trips as frequently as a gasoline car. This is another area where telematics can help, as it accurately tracks your mileage.

Multi Policy and Bundling Discounts

This isn't exclusive to EVs, but it's always a smart move. Bundling your auto insurance with other policies like home, renters, or even life insurance with the same provider can lead to significant savings. Most major insurers, including GEICO, Progressive, State Farm, and Allstate, offer substantial multi-policy discounts. If you're getting an EV, it's a great time to review all your insurance needs.

Good Driver and Defensive Driving Course Discounts

Maintaining a clean driving record is always the best way to save on insurance, regardless of your vehicle type. Many insurers offer good driver discounts for those with no accidents or violations for a certain period. Additionally, completing a defensive driving course can sometimes earn you a discount, especially if you're a younger driver or have had a minor infraction in the past. These apply equally to EV owners.

Comparing Top Auto Insurance Providers for EVs Insurer Reviews

Now, let's talk about some of the big players in the insurance game and how they stack up for EV owners in the USA. Keep in mind that rates and specific offerings can vary widely by state and individual circumstances, so always get multiple quotes!

Tesla Insurance Direct EV Coverage

It's hard to talk about EVs without mentioning Tesla. Tesla itself offers its own insurance product, currently available in several states (California, Texas, Arizona, Colorado, Illinois, Maryland, Nevada, Ohio, Oregon, Virginia). The big draw here is that Tesla Insurance is designed specifically for Tesla vehicles, leveraging real-time driving data from the car itself to calculate premiums. This means if you're a safe Tesla driver, you could see significant savings. They claim to offer rates 20-30% lower than competitors. However, it's only for Teslas, and availability is limited. If you own a Tesla and live in an eligible state, it's definitely worth checking out.

Progressive Snapshot and EV Discounts

Progressive is a giant in the insurance world, and their Snapshot program is well-known. This usage-based insurance program tracks your driving habits and can lead to discounts for safe drivers. For EV owners, this can be a great way to save, especially if your electric car encourages a smoother, more controlled driving style. Progressive also offers various standard discounts that EVs often qualify for, such as multi-policy and good driver discounts. They are generally competitive for a wide range of vehicles, including EVs.

GEICO Affordable EV Options

GEICO is famous for its competitive rates and ease of online quoting. They don't have specific 'EV discounts' per se, but their overall low-cost structure often makes them a strong contender for EV owners. They offer discounts for good drivers, multi-car policies, and various safety features that are common in EVs. Their online platform makes it super easy to get a quote and compare options quickly. If you're looking for straightforward, affordable coverage, GEICO is a solid choice.

State Farm Drive Safe & Save for Electric Cars

State Farm is another major insurer with a strong presence across the USA. Their Drive Safe & Save program is similar to Progressive's Snapshot, using telematics to reward safe driving. This can be very beneficial for EV owners who tend to drive more conservatively. State Farm also has a vast network of agents, which can be a plus if you prefer in-person service and personalized advice. They offer a wide array of discounts, including those for vehicle safety features and bundling.

Allstate Drivewise and EV Protection

Allstate's Drivewise program also uses telematics to personalize your rates based on your driving habits. They also offer a 'new car replacement' option, which can be particularly valuable for new EV owners, as it replaces your totaled new car with a brand new one (not just its depreciated value). Allstate also has a strong reputation for customer service and claims handling, which is important when dealing with potentially complex EV repairs. They offer various discounts that can apply to EVs, including those for anti-lock brakes and anti-theft devices.

Farmers Insurance Green Vehicle Discounts

Farmers Insurance is known for its comprehensive coverage options and personalized service. They are one of the insurers that explicitly offer a 'green vehicle' discount, which can apply to EVs. This is a direct saving for choosing an electric car. Farmers also offers new car replacement coverage and a variety of other discounts that can make them a competitive option for EV owners. Their agents can help you navigate the specific needs of insuring an electric vehicle.

Travelers Insurance EV Incentives

Travelers is another insurer that has shown support for green initiatives. They often provide discounts for hybrid and electric vehicles, making them an attractive option for EV owners. Travelers also offers a 'Premier New Car Replacement' option, which can be a great benefit for new EVs. They have a strong financial rating and offer a wide range of coverage options, including those for personal property and rental car reimbursement, which can be useful during EV repairs.

Specific EV Models and Their Insurance Costs Case Studies

Let's get a bit more specific. While it's impossible to give exact quotes without your personal details, we can look at general trends for some popular EV models.

Tesla Model 3 Insurance Cost Analysis

The Tesla Model 3 is one of the best-selling EVs in the USA. Its insurance costs can be a mixed bag. On one hand, it's packed with advanced safety features (Autopilot, collision avoidance) that can lead to discounts. On the other hand, its high-tech components and aluminum body can make repairs expensive. If you opt for Tesla Insurance, you might see lower rates. Otherwise, expect it to be slightly higher than a comparable gasoline-powered luxury sedan, but not astronomically so. For example, a 2023 Tesla Model 3 might cost around $1,800 - $2,500 per year to insure, depending on your location and driving record. This is often comparable to a BMW 3 Series or Audi A4.

Ford Mustang Mach-E Insurance Comparison

The Ford Mustang Mach-E is a popular electric SUV that blends performance with practicality. Its insurance costs tend to be in line with other mid-size SUVs, perhaps a bit higher due to its advanced technology and performance capabilities. Ford's extensive dealer network might make repairs slightly more accessible than some other EV brands, potentially influencing rates positively. A 2023 Ford Mustang Mach-E could range from $1,700 - $2,300 annually for insurance. This is often similar to a Ford Edge ST or a higher trim Toyota RAV4.

Nissan Leaf Insurance Affordability

The Nissan Leaf is often considered one of the more affordable EVs, and its insurance costs usually reflect that. It's less performance-oriented and has been around longer, meaning repair networks are more established. This can translate to lower premiums. If you're looking for an entry-level EV with manageable insurance costs, the Leaf is a strong contender. A 2023 Nissan Leaf might cost around $1,500 - $2,000 per year to insure, often comparable to a Honda Civic or Toyota Corolla.

Hyundai Ioniq 5 Insurance Considerations

The Hyundai Ioniq 5 has gained a lot of popularity for its unique styling and impressive range. Its insurance costs are generally competitive, falling somewhere between the Leaf and the Model 3. Hyundai's growing EV infrastructure and warranty support can be beneficial. Its advanced safety features will likely qualify for discounts. Expect annual insurance costs for a 2023 Hyundai Ioniq 5 to be in the range of $1,600 - $2,200, similar to a Hyundai Santa Fe or Kia Sorento.

Rivian R1T and R1S Insurance for Electric Trucks and SUVs

Rivian's R1T electric pickup truck and R1S SUV represent a newer segment of the EV market. As luxury, high-performance electric trucks/SUVs, their insurance costs tend to be on the higher side. Their specialized components, limited repair network (for now), and higher purchase price contribute to this. Expect insurance for a Rivian R1T or R1S to be in the higher range, potentially $2,500 - $3,500+ annually, comparable to other luxury trucks or large SUVs like a high-trim Ford F-150 or a Land Rover Defender.

Tips for Getting the Best EV Auto Insurance Rates Smart Shopping

So, how do you make sure you're getting the best deal on your EV insurance? Here are some pro tips:

Shop Around and Compare Multiple Quotes

This is the golden rule for any insurance, but especially important for EVs where offerings can vary. Don't just stick with your current provider. Get quotes from at least 3-5 different insurance companies. Use online comparison tools, or work with an independent insurance agent who can shop multiple carriers for you. Companies like Policygenius, The Zebra, and NerdWallet can help you compare quotes side-by-side.

Inquire About EV Specific Discounts

When you're getting quotes, explicitly ask about any discounts for electric vehicles, green vehicles, or advanced safety features. Don't assume they'll automatically apply them. Be your own advocate!

Consider a Higher Deductible

If you have a healthy emergency fund, opting for a higher deductible (e.g., $1,000 instead of $500) can significantly lower your monthly or annual premiums. Just make sure you can comfortably afford to pay that deductible out of pocket if you need to file a claim.

Maintain a Clean Driving Record

This goes without saying, but avoiding accidents and traffic violations is the single best way to keep your insurance rates low, regardless of your vehicle type. Safe driving pays off, literally.

Bundle Your Policies

As mentioned, combining your auto insurance with your home, renters, or other insurance policies with the same provider can lead to substantial savings. It's often one of the biggest discounts you can get.

Utilize Telematics Programs

If you're a safe driver, consider enrolling in a usage-based insurance program like Progressive Snapshot or State Farm Drive Safe & Save. These programs can reward your good driving habits with lower premiums.

Review Your Coverage Annually

Your insurance needs can change over time. Review your policy at least once a year to ensure you still have the right amount of coverage and that you're not overpaying. As your EV ages, its value might decrease, and you might be able to adjust your comprehensive and collision coverage accordingly.

Ask About OEM Parts Coverage

For EVs, especially newer models, using Original Equipment Manufacturer (OEM) parts for repairs can be crucial for maintaining performance and warranty. Some policies might default to aftermarket parts. Ask your insurer if they offer OEM parts coverage, or if it's included in your policy, especially for critical EV components.

The Future of EV Auto Insurance Trends and Innovations

The EV market is evolving rapidly, and so is the insurance industry's approach to it. Here's a peek at what's on the horizon:

More Specialized EV Insurance Products

Expect to see more insurance companies offering highly specialized EV insurance products, similar to Tesla Insurance. These policies will likely leverage even more real-time data from the vehicle and offer tailored coverage for batteries, charging equipment, and software updates.

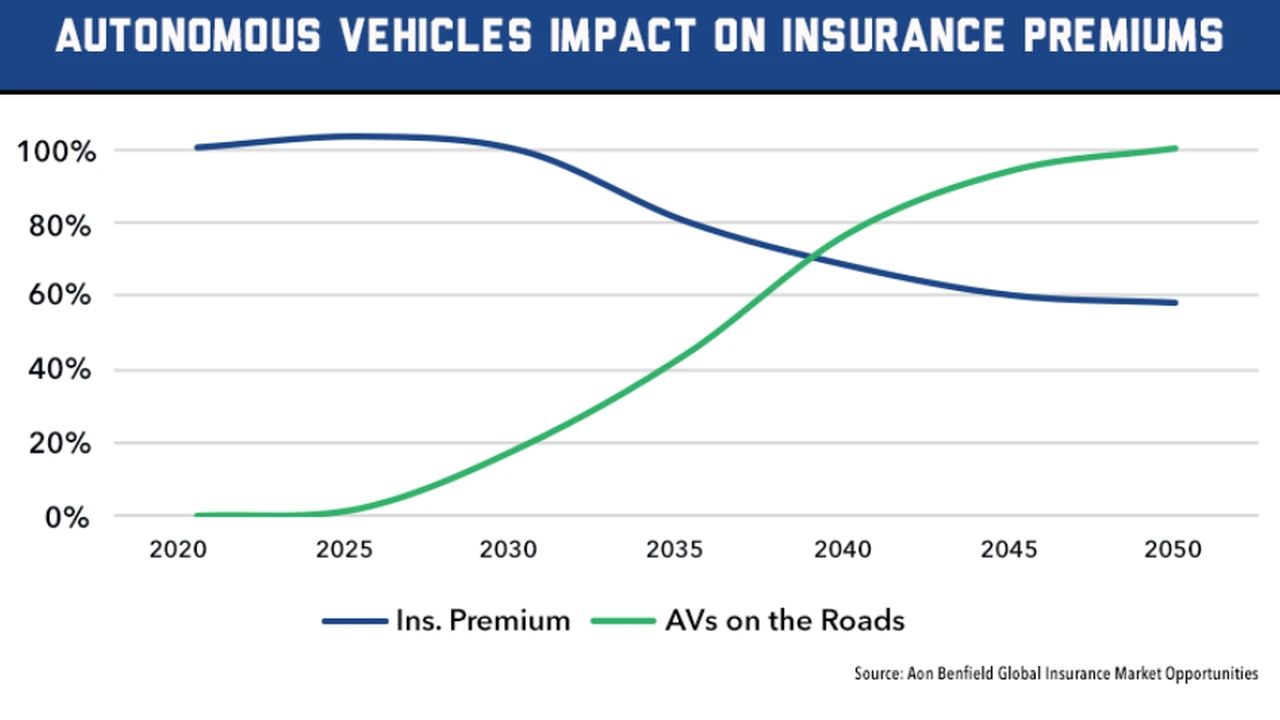

Increased Focus on ADAS and Autonomous Features

As EVs become even more autonomous, the liability landscape will shift. Insurers will increasingly factor in the capabilities of advanced driver-assistance systems and, eventually, fully autonomous driving systems. This could lead to new types of coverage and potentially lower premiums as accident rates theoretically decrease.

Dynamic Pricing Based on Driving Behavior

Telematics will become even more sophisticated, leading to more dynamic pricing models. Your premium might adjust more frequently based on your actual driving behavior, rather than just at renewal time. This could be a huge win for safe EV drivers.

Partnerships with EV Manufacturers and Repair Networks

Insurers will likely forge stronger partnerships with EV manufacturers and certified repair shops to streamline the claims process and ensure quality repairs. This could lead to more efficient and cost-effective repairs for EV owners.

Cybersecurity Coverage for Connected Cars

As EVs become more connected and reliant on software, cybersecurity risks could emerge. We might see new insurance products that offer coverage for cyberattacks or data breaches related to your vehicle's systems. It's a brave new world out there!

Insuring an electric vehicle in the USA is a bit different from insuring a traditional car, but it's far from complicated. By understanding the unique coverage needs, leveraging available discounts, and shopping around, you can find a policy that provides excellent protection without breaking the bank. The EV revolution is here to stay, and the insurance industry is adapting right along with it. So, drive safe, enjoy your electric ride, and make sure you're well-covered!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)