Comparing Auto Insurance Options in Thailand

Explore comparing auto insurance options in Thailand. Understand local regulations and find the best coverage for your car in Thailand.

Explore comparing auto insurance options in Thailand. Understand local regulations and find the best coverage for your car in Thailand.

Comparing Auto Insurance Options in Thailand

Understanding Thai Auto Insurance Types and Coverage

Navigating the world of auto insurance in Thailand can feel a bit like driving on a busy Bangkok street – exciting, a little chaotic, and full of unexpected turns! But don't worry, we're here to help you understand the different types of coverage available, what local regulations mean for you, and how to find the best policy for your beloved vehicle. Whether you're a local resident, an expat, or just someone looking to buy a car here, getting the right insurance is super important. It's not just about following the law; it's about protecting your finances and giving you peace of mind.

In Thailand, auto insurance is generally categorized into two main types: Compulsory Motor Insurance (CMI), also known as Por Ror Bor (พ.ร.บ.), and Voluntary Motor Insurance. Let's break them down.

Compulsory Motor Insurance CMI Por Ror Bor Explained

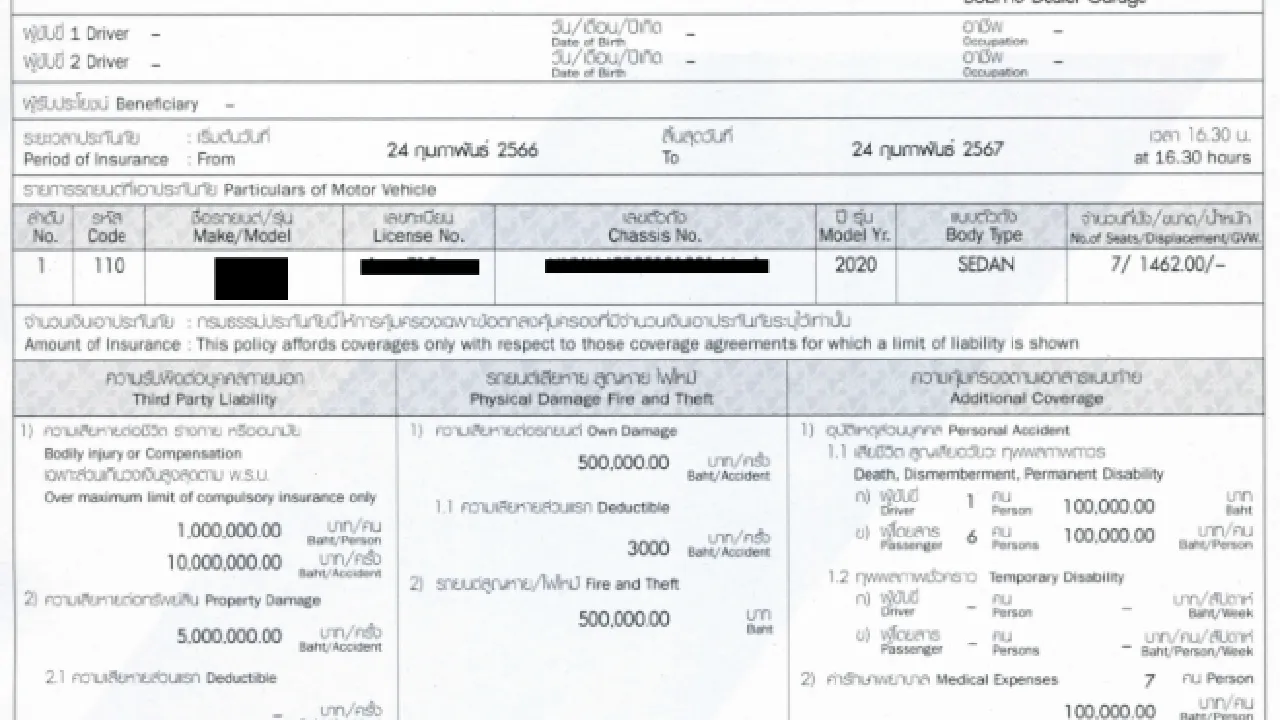

Every single vehicle on Thai roads, from a scooter to a luxury sedan, must have Compulsory Motor Insurance (CMI), or Por Ror Bor. This isn't optional; it's the law. Think of it as the absolute bare minimum. Its primary purpose is to provide basic protection for victims of road accidents, regardless of who was at fault. It covers medical expenses and compensation for injury or death for all parties involved in an accident, including the driver, passengers, and third parties. However, it doesn't cover damage to vehicles or property. The coverage limits are relatively low, so while it's essential, it's definitely not enough on its own for comprehensive protection.

For example, as of my last update, the CMI typically covers medical expenses up to a certain amount per person per accident, and a lump sum for death or permanent disability. These figures are set by the government and can change, so it's always good to check the latest regulations. You usually get your CMI when you renew your annual road tax, and it's a pretty straightforward process.

Voluntary Motor Insurance Types and Benefits

This is where things get interesting and where you can really tailor your protection. Voluntary motor insurance in Thailand comes in several 'classes,' each offering different levels of coverage. These classes are numbered, with Class 1 offering the most comprehensive protection and higher numbers offering more limited coverage.

Class 1 Auto Insurance The Most Comprehensive Coverage

Class 1 is the crème de la crème of auto insurance in Thailand. It's often referred to as 'full coverage' and is highly recommended, especially for newer or more expensive vehicles. It covers pretty much everything:

- Own Damage (OD): This is a big one. It covers damage to your own vehicle, even if you're at fault in an accident. This includes collisions, overturning, and even damage from natural disasters like floods or fires.

- Third-Party Liability (TPL): Covers damage to other vehicles or property, and medical expenses/death for third parties. This is usually much higher than CMI limits.

- Theft: If your car gets stolen, Class 1 will cover it.

- Fire: Protection against fire damage to your vehicle.

- Personal Accident (PA): Covers medical expenses and compensation for injury or death for the driver and passengers in your car.

- Medical Expenses: Similar to PA, but specifically for medical treatment.

- Bail Bond: If you're involved in an accident and need to be bailed out, this coverage can help.

Class 1 is the most expensive option, but it offers the most peace of mind. It's particularly popular for new cars, luxury vehicles, and for drivers who want maximum protection against unforeseen events.

Class 2+ Auto Insurance A Popular Mid Range Option

Class 2+ is a very popular choice for many Thai drivers, offering a good balance between coverage and cost. It's like a slightly scaled-down version of Class 1. It typically covers:

- Damage to your own vehicle in the event of a collision with another vehicle (where the other vehicle is identifiable).

- Third-Party Liability (TPL).

- Theft.

- Fire.

- Personal Accident (PA) and Medical Expenses for occupants.

- Bail Bond.

The key difference from Class 1 is that Class 2+ usually does not cover damage to your own vehicle if you hit an inanimate object (like a tree or a wall) or if the other vehicle involved in a collision cannot be identified (e.g., a hit-and-run where you can't provide details of the other car). It's a great option for older cars or for drivers who want more than basic coverage but find Class 1 too pricey.

Class 3+ Auto Insurance Basic Collision and Third Party

Class 3+ is a step down from 2+. It focuses on third-party liability and damage to your own vehicle in a collision with another identifiable vehicle. It generally includes:

- Third-Party Liability (TPL).

- Damage to your own vehicle in a collision with another identifiable vehicle.

- Personal Accident (PA) and Medical Expenses for occupants.

- Bail Bond.

What's usually missing here compared to 2+ is coverage for theft and fire. It's a more budget-friendly option for those who are primarily concerned with covering damage from collisions with other cars and third-party costs.

Class 2 Auto Insurance Theft and Fire Focus

Class 2 insurance is a bit unique. It primarily covers theft and fire damage to your own vehicle, along with third-party liability. It typically does not cover damage to your own vehicle from collisions. This might be suitable for someone who has an older car that isn't worth much in terms of collision repair but wants protection against theft or fire.

Class 3 Auto Insurance The Most Basic Voluntary Coverage

Class 3 is the most basic voluntary insurance. It only covers third-party liability for property damage and bodily injury/death. It does not cover any damage to your own vehicle, nor does it cover theft or fire. This is the cheapest voluntary option and is usually chosen for very old cars where the owner is willing to bear the cost of their own vehicle's repairs in an accident.

Key Factors to Consider When Choosing Auto Insurance in Thailand

Choosing the right insurance isn't just about picking a class. There are several other factors that will influence your decision and the premium you pay.

Vehicle Type Age and Value Impact on Premiums

The type of car you drive plays a huge role. A brand-new Mercedes-Benz will naturally cost more to insure than a 10-year-old Honda City. Why? Because the repair costs for a luxury car are much higher, and its market value is greater. Insurers also look at the car's age. Older cars might not qualify for Class 1 insurance, or the premium might be disproportionately high compared to the car's value. The value of your car directly impacts the sum insured, which is the maximum amount the insurer will pay out for damage or total loss.

Driver Profile and Driving History Discounts and Surcharges

Your personal profile matters. Younger, less experienced drivers often face higher premiums because they are statistically more likely to be involved in accidents. Conversely, drivers with a clean driving record (no claims for several years) can often get a 'No Claims Discount' (NCD), which can significantly reduce your premium. Some insurers might also consider your occupation or even where you park your car overnight (e.g., in a secure garage vs. on the street).

Coverage Limits and Deductibles Understanding Your Financial Exposure

When you get a quote, pay close attention to the coverage limits for third-party liability (both bodily injury and property damage) and the sum insured for your own vehicle. Higher limits offer more protection but come with a higher premium. The deductible (or 'excess' as it's sometimes called) is the amount you agree to pay out of pocket for each claim before the insurance kicks in. A higher deductible usually means a lower premium, but it also means you'll pay more if you have to make a claim. It's a balancing act between saving on premiums and being prepared for potential out-of-pocket costs.

Additional Riders and Optional Benefits Enhancing Your Policy

Many insurers offer optional add-ons or 'riders' that can enhance your policy. These might include:

- Roadside Assistance: For breakdowns, flat tires, or running out of fuel.

- Car Rental: Provides a rental car while yours is being repaired after an accident.

- Flood Coverage: Essential in many parts of Thailand during the rainy season.

- Terrorism Coverage: While hopefully never needed, some policies offer this.

- Personal Belongings Coverage: For items stolen from your car.

Consider which of these are important for your lifestyle and peace of mind. Adding them will increase your premium, but they can be invaluable in an emergency.

Top Auto Insurance Providers in Thailand and Their Offerings

Thailand has a competitive insurance market with many reputable local and international players. Here are a few prominent ones, along with a general idea of what they offer. Please note that specific product names, features, and pricing can change, so always get a direct quote.

AXA Insurance Thailand Comprehensive and Reliable

AXA is a global insurance giant with a strong presence in Thailand. They are known for their comprehensive Class 1 policies, often favored by expats and those with newer, higher-value vehicles. They offer a range of voluntary insurance options, including Class 1, 2+, and 3+. AXA often provides good customer service and has a relatively straightforward claims process. Their Class 1 policies typically include extensive coverage for own damage, third-party liability, theft, fire, and personal accident benefits. They also offer various add-ons like roadside assistance and flood coverage. Their pricing tends to be competitive for the level of coverage provided, often appealing to those who prioritize reliability and a smooth claims experience.

Viriyah Insurance Thailand The Market Leader

Viriyah Insurance is often considered the largest and most popular auto insurer in Thailand. They have an extensive network of branches and repair centers across the country, which can be a huge advantage when making a claim, especially outside of major cities. Viriyah offers all classes of voluntary insurance (Class 1, 2+, 3+, 2, 3) and is known for its competitive pricing, particularly for Class 2+ and 3+ policies. They are a go-to for many Thai drivers due to their widespread presence and efficient claims handling. Their Class 1 policies are robust, and they are often a strong contender for those seeking a balance of cost and accessibility.

Bangkok Insurance Thailand Strong Local Presence

Bangkok Insurance is another well-established Thai insurer with a long history and a solid reputation. They offer a full suite of auto insurance products, from Class 1 to Class 3. They are known for their strong financial backing and reliable service. Bangkok Insurance often provides good options for both individual and corporate clients. Their policies are generally comprehensive, and they have a good network of garages. They are a reliable choice for those looking for a trusted local provider with a strong track record.

Dhipaya Insurance Thailand Government Backed Option

Dhipaya Insurance is a state-owned enterprise, which gives it a certain level of trust and stability. They offer a wide range of auto insurance products, including all classes of voluntary insurance. Dhipaya is often competitive on pricing and provides good coverage options. They are a popular choice for government employees and those who prefer a state-backed insurer. Their claims process is generally efficient, and they have a good reputation for customer service.

MSIG Insurance Thailand International Standards

MSIG is an international insurer with a significant presence in Southeast Asia, including Thailand. They are known for offering policies that meet international standards, which can be appealing to expats. MSIG provides comprehensive Class 1 coverage, as well as other classes. They often focus on providing clear policy terms and good customer support, with a focus on English-speaking services for their international clientele. Their pricing might be slightly higher than some local competitors, but this is often justified by their service quality and international backing.

Comparing Specific Products and Scenarios

Let's look at some specific scenarios and how different insurance products might compare.

Scenario 1 New Car Owner in Bangkok

Vehicle: Brand new Honda Civic, valued at 900,000 THB.

Driver: 30-year-old professional, clean driving record.

Usage: Daily commute in Bangkok, occasional weekend trips.

Recommendation: Class 1 Auto Insurance.

- AXA Class 1: Might offer a premium around 20,000 - 25,000 THB per year, with a low deductible (e.g., 1,000 THB). Includes comprehensive own damage, high third-party limits (e.g., 10 million THB for bodily injury, 2.5 million THB for property damage), theft, fire, flood, and roadside assistance.

- Viriyah Class 1: Similar premium range, perhaps slightly lower at 19,000 - 24,000 THB. Excellent network of garages, which is a big plus in Bangkok. Coverage would be comparable to AXA.

- Bangkok Insurance Class 1: Likely in the 20,000 - 26,000 THB range. Known for reliable service and good claims handling.

Why Class 1? For a new car, the investment is significant. Class 1 protects against all types of damage to your own vehicle, including those where you're at fault or no other party is involved. The peace of mind is worth the higher premium.

Scenario 2 Used Car Owner in Chiang Mai

Vehicle: 7-year-old Toyota Vios, valued at 300,000 THB.

Driver: 45-year-old, drives moderately, 3 years No Claims Discount.

Usage: Daily errands, occasional longer drives.

Recommendation: Class 2+ Auto Insurance.

- Viriyah Class 2+: Premium might be around 10,000 - 14,000 THB per year, with a deductible of 3,000 - 5,000 THB. Covers collision with identifiable vehicles, third-party liability, theft, and fire. Their extensive network is great for Chiang Mai.

- Dhipaya Class 2+: Potentially slightly lower, 9,500 - 13,500 THB. Good coverage for the price, reliable.

- AXA Class 2+: Might be 11,000 - 15,000 THB. Good for those who prefer an international brand, but Viriyah might have a slight edge on local network.

Why Class 2+? The car's value doesn't warrant the full expense of Class 1, but the owner still wants protection against common risks like collisions, theft, and fire. The deductible helps keep the premium down.

Scenario 3 Budget Conscious Driver in Pattaya

Vehicle: 12-year-old Isuzu D-Max pickup truck, valued at 150,000 THB.

Driver: 55-year-old, careful driver, limited budget.

Usage: Local driving, transporting goods.

Recommendation: Class 3+ or Class 3 Auto Insurance.

- Viriyah Class 3+: Premium around 6,000 - 8,000 THB. Covers third-party liability and own damage from collision with identifiable vehicles. No theft or fire.

- Bangkok Insurance Class 3: Premium around 3,500 - 5,000 THB. Only covers third-party liability. No own damage, theft, or fire.

Why Class 3+ or 3? For an older, lower-value vehicle, the cost of comprehensive insurance might exceed the car's worth. Class 3+ offers basic collision coverage for your own vehicle, while Class 3 focuses solely on protecting you from third-party claims, which can be financially devastating. The owner is willing to self-insure for minor damage to their own vehicle.

Tips for Finding the Best Auto Insurance in Thailand

Don't just jump at the first offer! Here's how to be a savvy insurance shopper in Thailand.

Compare Multiple Quotes Online and Through Brokers

This is probably the most important tip. Never settle for just one quote. Use online comparison websites (though these are less prevalent and comprehensive in Thailand compared to Western countries, some local ones exist), or better yet, contact a few different insurance brokers. Brokers work with multiple insurance companies and can often find you better deals or policies that perfectly match your needs. They can also explain the nuances of different policies in English, which is a huge help.

Read the Fine Print Policy Exclusions and Conditions

Insurance policies can be dense, but it's crucial to understand what's covered and, more importantly, what's not covered. Pay attention to exclusions (e.g., certain types of damage, specific driving conditions), conditions (e.g., requirements for reporting an accident), and the claims process. If you don't understand something, ask your broker or the insurance company directly. Don't assume anything!

Check the Insurer's Reputation and Claims Service

A cheap premium is great, but it's useless if the insurance company is difficult to deal with when you need to make a claim. Look for insurers with a good reputation for customer service and efficient claims handling. Online reviews, expat forums, and recommendations from friends can be valuable resources. A good claims service means less stress and faster resolution when you're already dealing with the aftermath of an accident.

Consider Your Driving Habits and Risk Tolerance

Be honest with yourself about how you drive and your risk tolerance. If you're a very careful driver with a low-value car, you might be comfortable with a higher deductible or a Class 2+ policy. If you're driving a brand-new SUV in heavy city traffic, a comprehensive Class 1 policy with a low deductible is probably a smarter choice. Your insurance should reflect your actual needs and comfort level with risk.

Don't Forget About Roadside Assistance and Other Add Ons

While these add-ons increase your premium, they can be incredibly useful. Thailand's roads can be challenging, and having roadside assistance can save you a lot of hassle and expense if you break down. Consider if the convenience and peace of mind offered by these extras are worth the additional cost for your specific situation.

The Claims Process in Thailand What to Expect

Knowing what to do after an accident can make a stressful situation much easier. Here's a general overview of the claims process in Thailand.

Immediate Steps After an Accident Safety First

First and foremost, ensure everyone's safety. Move your vehicle to a safe location if possible. Then, call your insurance company immediately. Most Thai insurers have a 24/7 hotline. They will dispatch a claims adjuster to the scene. Do not move your vehicle from the accident spot if there are injuries or significant damage, unless it's absolutely necessary for safety. Take photos and videos of the accident scene, vehicle damage, and any relevant road signs or conditions. Exchange contact and insurance information with the other parties involved. If there are injuries or significant damage, you should also call the police (191).

Working with the Claims Adjuster On Site Assessment

The claims adjuster will arrive at the scene to assess the damage, take statements, and determine initial liability. They will guide you through the necessary paperwork. Be cooperative and provide all requested information. If you have a Class 1 policy, the adjuster will often issue a 'claim report' that allows you to take your car to an authorized garage for repairs. For other classes, the process might vary slightly depending on the nature of the claim.

Repair Process and Settlement Getting Your Car Fixed

Once the claim is approved, you'll take your car to an approved garage for repairs. For Class 1 policies, the insurer usually covers the repair costs directly with the garage, minus your deductible. For other classes, or if you're claiming against a third party, the process might involve more direct communication between the insurers. For total loss situations, the insurer will pay out the agreed-upon sum insured, minus any deductible. The settlement process can take time, especially for complex cases or those involving injuries, so patience is key.

Final Thoughts on Auto Insurance in Thailand

Getting auto insurance in Thailand doesn't have to be a headache. By understanding the different types of coverage, considering your personal needs, and comparing options from reputable providers, you can find a policy that offers excellent protection without breaking the bank. Remember, the cheapest option isn't always the best. Prioritize comprehensive coverage, especially for newer vehicles, and choose an insurer known for reliable claims service. Drive safely, and enjoy the beautiful roads of Thailand with confidence!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)