Comparing Auto Insurance Rates Across US States

Explore comparing auto insurance rates across US states. Understand how location impacts your premiums and find the most affordable states.

Explore comparing auto insurance rates across US states. Understand how location impacts your premiums and find the most affordable states.

Comparing Auto Insurance Rates Across US States Your Ultimate Guide to Location Based Savings

Ever wondered why your friend in Ohio pays so much less for car insurance than you do in Florida, even though you drive similar cars and have clean records? It's not just your imagination. Auto insurance rates vary wildly from state to state across the USA. This isn't some random lottery; it's a complex calculation based on a multitude of factors unique to each state. Understanding these differences can be a game-changer for your wallet, especially if you're considering a move or just want to know if you're getting a fair deal.

Why Do Auto Insurance Rates Differ So Much By State Understanding the Core Factors

The primary reason for such significant rate disparities lies in a combination of state-specific regulations, environmental factors, population density, and even local driving habits. Let's break down the key elements:

State Regulations and Minimum Coverage Requirements The Legal Landscape

Every state sets its own minimum auto insurance requirements. Some states, like New Hampshire, don't even mandate auto insurance, though financial responsibility is still required. Others, like Michigan, historically had some of the highest minimums due to their no-fault system and unlimited personal injury protection (PIP) benefits, though recent reforms have brought some changes. These minimums directly impact the baseline cost of insurance. States with higher minimum liability limits or additional mandatory coverages (like PIP or uninsured motorist coverage) will naturally have higher average premiums.

Accident Rates and Claims Frequency The Risk Factor

Insurance companies are all about risk assessment. States with higher accident rates, more frequent claims, or a greater number of severe accidents will see higher premiums. This can be influenced by factors like:

- Population Density and Traffic Congestion: More cars on the road, especially in urban areas, mean a higher likelihood of accidents. States with large metropolitan areas often have higher rates.

- Road Conditions and Infrastructure: Poorly maintained roads or challenging driving conditions (e.g., mountainous terrain, frequent snow/ice) can contribute to more accidents.

- Driving Habits: Aggressive driving, speeding, or a higher incidence of distracted driving in a particular state can push rates up.

Cost of Repairs and Medical Care The Economic Impact

The cost of repairing vehicles and providing medical care for accident victims also plays a huge role. If labor costs for mechanics are higher in one state, or if medical treatments are more expensive, insurance companies will factor that into their premiums. This is particularly true in states with higher costs of living overall.

Weather and Natural Disasters The Environmental Influence

States prone to severe weather events like hurricanes (Florida, Louisiana), hailstorms (Texas, Oklahoma), wildfires (California), or blizzards (Northeast, Midwest) will have higher comprehensive coverage costs. Insurers account for the increased risk of damage from these natural phenomena.

Theft and Vandalism Rates The Crime Component

If a state or specific areas within a state have high rates of car theft or vandalism, comprehensive coverage premiums will be higher. Insurers analyze crime statistics to determine this risk.

Competition Among Insurers The Market Dynamics

The number of insurance companies operating in a state and the level of competition among them can also affect rates. More competition generally leads to more competitive pricing, while fewer options might result in higher premiums.

The Most Expensive States for Auto Insurance Where Your Dollar Goes Further

While averages can fluctuate, certain states consistently rank among the most expensive for auto insurance. These often share characteristics like high population density, severe weather risks, or specific regulatory environments.

Michigan A Historical Look at High Costs

For many years, Michigan held the unenviable title of the most expensive state for auto insurance. This was largely due to its unique no-fault system, which mandated unlimited lifetime personal injury protection (PIP) benefits. While reforms in 2020 aimed to reduce these costs, Michigan still remains on the higher end due to lingering effects and other contributing factors.

Florida The Sunshine State's High Premiums

Florida is another state known for its high auto insurance rates. A combination of factors contributes to this: a high number of uninsured drivers, frequent hurricanes and tropical storms (leading to higher comprehensive claims), a high population of elderly drivers (who statistically have more accidents), and a significant number of fraudulent claims. The state's no-fault system also plays a role.

Louisiana The Bayou State's Insurance Burden

Louisiana consistently ranks among the most expensive. Factors include a high rate of uninsured motorists, a litigious environment (more lawsuits after accidents), frequent severe weather (hurricanes, floods), and poor road conditions in some areas.

New York The Empire State's Urban Surcharge

New York's high rates are heavily influenced by its dense urban areas, particularly New York City. High traffic volume, increased accident risk, higher repair costs, and a significant number of uninsured drivers contribute to the elevated premiums.

California The Golden State's Complexities

California's rates are driven by its massive population, high traffic congestion, expensive repair costs, and the increasing risk of wildfires. While not always the absolute highest, it consistently ranks among the more expensive states, especially in metropolitan areas.

The Most Affordable States for Auto Insurance Finding Your Savings Sweet Spot

On the flip side, some states consistently offer more affordable auto insurance rates. These states often have lower population densities, fewer severe weather events, or more favorable regulatory environments.

Maine The Pine Tree State's Pleasant Premiums

Maine frequently appears on lists of the most affordable states for auto insurance. It benefits from a lower population density, fewer large urban centers, and a relatively low rate of car theft and accidents.

New Hampshire Live Free and Insure Cheaply

New Hampshire is unique because it doesn't legally require auto insurance, though drivers must still prove financial responsibility. This lack of mandate, combined with a lower population density and fewer major metropolitan areas, contributes to lower average premiums for those who do choose to purchase coverage.

Idaho The Gem State's Gentle Rates

Idaho offers some of the lowest rates in the country. Its rural nature, lower population density, and relatively low accident and theft rates contribute to its affordability.

Ohio The Buckeye State's Budget Friendly Options

Ohio often ranks as one of the more affordable states. It has a good balance of urban and rural areas, competitive insurance markets, and generally reasonable accident rates.

North Carolina The Tar Heel State's Tame Premiums

North Carolina benefits from a strong regulatory environment that helps keep rates in check, along with a lower population density compared to some of its more expensive neighbors.

Specific Product Recommendations and Comparisons Navigating the Market

When comparing auto insurance across states, it's not just about the state average; it's about finding the right provider for your specific needs. Here are some top-tier providers known for their competitive rates, strong customer service, and broad coverage options, along with considerations for different scenarios.

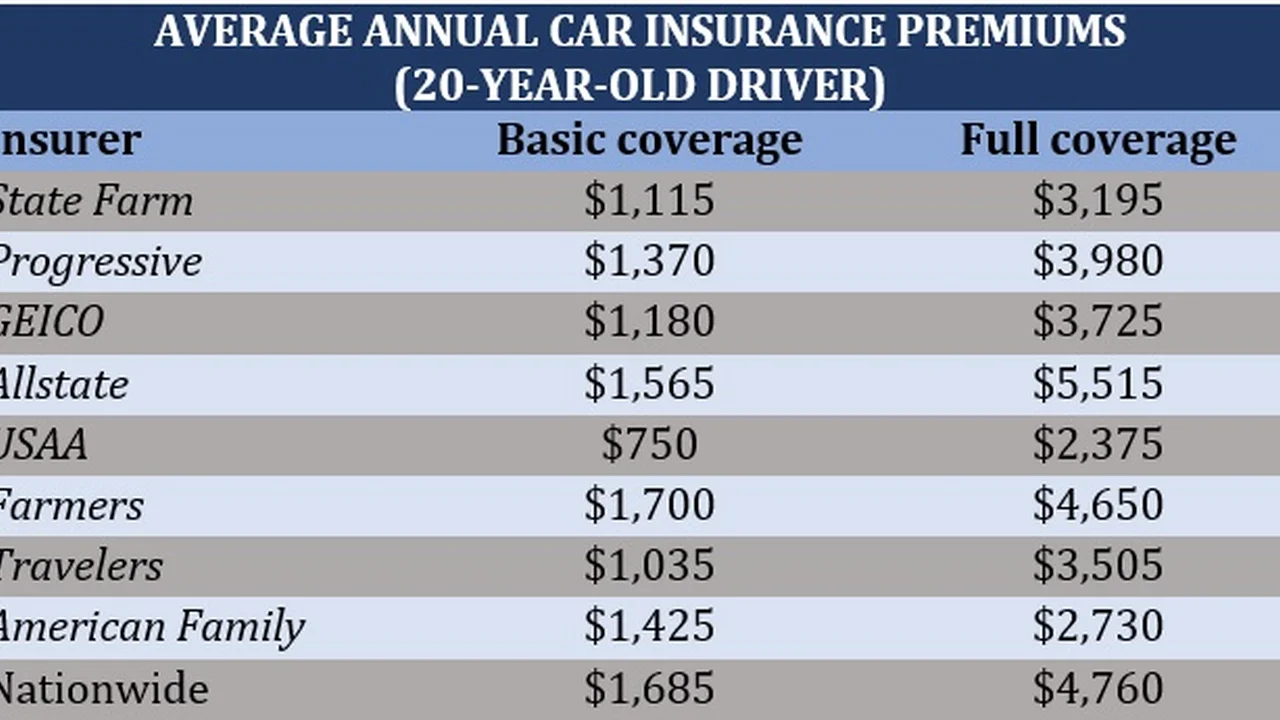

For Overall Value and Broad Coverage Geico Progressive and State Farm

These three giants consistently rank high for their competitive pricing, extensive discount options, and widespread availability across most US states. They are excellent starting points for comparison, regardless of your location.

Geico

- Strengths: Known for aggressive pricing, especially for drivers with clean records. Excellent online and mobile experience. Offers a wide array of discounts (multi-car, good student, federal employee, military, etc.).

- Best For: Drivers looking for a straightforward, affordable policy with strong digital tools. Often very competitive in states like Virginia, Arizona, and Texas.

- Considerations: While customer service is generally good, some prefer a more personalized agent experience.

- Typical Annual Premium Range: $1,200 - $2,500 (highly dependent on state, driver profile, and coverage).

Progressive

- Strengths: Famous for its Name Your Price tool and Snapshot program (usage-based insurance). Offers many unique discounts and is often competitive for drivers with less-than-perfect records. Strong online presence.

- Best For: Drivers who want to customize their policy, those open to telematics for potential savings, and drivers in states like Florida, Georgia, and Pennsylvania where they often have strong market penetration.

- Considerations: Snapshot requires sharing driving data, which isn't for everyone.

- Typical Annual Premium Range: $1,300 - $2,800.

State Farm

- Strengths: Largest auto insurer in the US, known for its extensive network of local agents. Offers personalized service and a wide range of insurance products (bundling opportunities). Strong financial stability.

- Best For: Drivers who prefer an in-person agent experience, those looking to bundle multiple insurance policies, and often competitive in states like Illinois, Indiana, and Kansas.

- Considerations: May not always be the cheapest option, especially for online-savvy shoppers.

- Typical Annual Premium Range: $1,400 - $2,700.

For Customer Service and Claims Handling USAA and Amica

If top-notch customer service and a smooth claims process are your priority, these two often lead the pack.

USAA

- Strengths: Consistently ranks #1 for customer satisfaction. Offers highly competitive rates and specialized benefits for military members and their families. Exceptional claims handling.

- Best For: Active military, veterans, and their eligible family members. Available in all states.

- Considerations: Eligibility is restricted to the military community.

- Typical Annual Premium Range: $1,000 - $2,000 (often significantly lower than competitors for eligible members).

Amica Mutual

- Strengths: Known for outstanding customer service and high policyholder dividends (for mutual policyholders). Offers a wide range of coverage options and discounts.

- Best For: Drivers who prioritize excellent service and are willing to pay a slightly higher premium for it. Often competitive in states like Massachusetts, Connecticut, and Rhode Island.

- Considerations: May not be the cheapest option, and not available in all states.

- Typical Annual Premium Range: $1,500 - $3,000.

For High-Risk Drivers and Specialized Needs The General and National General

If you have a less-than-perfect driving record, these companies specialize in providing coverage where others might decline.

The General

- Strengths: Specializes in providing coverage for high-risk drivers (e.g., those with DUIs, multiple accidents, or poor credit). Offers SR-22 filings.

- Best For: Drivers who have difficulty getting insurance elsewhere due to their driving history. Available in most states.

- Considerations: Premiums will be higher due to the increased risk. Customer service reviews are mixed.

- Typical Annual Premium Range: $2,000 - $5,000+ (highly variable based on risk).

National General

- Strengths: Offers a variety of coverage options, including for high-risk drivers. Known for its RV and classic car insurance. Provides a SmartDrive program for usage-based savings.

- Best For: Drivers with unique insurance needs, including high-risk profiles, and those looking for specialized vehicle coverage. Available in most states.

- Considerations: Rates can be higher for standard policies compared to major competitors.

- Typical Annual Premium Range: $1,800 - $4,000+.

How to Compare Auto Insurance Rates Effectively Across States Your Action Plan

Comparing rates isn't just about getting a single quote. It's about a strategic approach to ensure you're getting the best value for your money, no matter which state you're in.

Get Multiple Quotes From Different Providers

This is the golden rule. Never settle for the first quote you receive. Use online comparison tools or contact independent agents who can shop around for you. Aim for at least 3-5 quotes.

Understand State Minimums and Your Coverage Needs

Before comparing, know what your state legally requires. Then, assess your personal needs. Do you need full coverage? What deductible are you comfortable with? Don't just compare apples to oranges; ensure you're comparing similar coverage levels.

Leverage All Available Discounts

Discounts can significantly reduce your premium. Common discounts include:

- Multi-policy/Bundling: Combining auto with home, renters, or life insurance.

- Good Driver: For drivers with a clean record over a certain period.

- Good Student: For young drivers with good academic performance.

- Defensive Driving Course: Completing an approved safety course.

- Vehicle Safety Features: For cars with anti-lock brakes, airbags, anti-theft devices.

- Low Mileage: If you don't drive much.

- Usage-Based Insurance (UBI): Programs like Progressive Snapshot or Geico DriveEasy that monitor driving habits.

Consider Your Deductible

A higher deductible (the amount you pay out-of-pocket before insurance kicks in) will lower your premium. Just make sure you can comfortably afford your chosen deductible if you need to file a claim.

Maintain a Good Credit Score

In most states (California, Hawaii, and Massachusetts are exceptions), insurers use credit scores as a factor in determining premiums. A better credit score often translates to lower rates.

Review Your Policy Annually

Life changes, and so should your insurance. Review your policy at least once a year, or whenever you have a major life event (new car, new address, marriage, new driver in the household). Your current insurer might not be the cheapest option anymore.

Ask About Specific State Programs or Rebates

Some states might have specific programs or rebates that can help lower costs, especially for certain demographics or vehicle types. An independent agent familiar with your state's market can be a great resource here.

The Impact of Moving States on Your Auto Insurance What to Expect

If you're planning a move across state lines, your auto insurance will almost certainly change. Here's what you need to know:

Notify Your Insurer Immediately

It's crucial to inform your insurance company as soon as you know you're moving. Your current policy might not be valid in your new state, or it might not meet the new state's minimum requirements. Failing to notify them could lead to a lapse in coverage or even legal issues.

Your Rates Will Likely Change

As we've discussed, rates vary significantly by state. Be prepared for your premium to go up or down depending on where you're moving from and to. For example, moving from Maine to Florida will almost certainly result in a higher premium.

You Might Need a New Insurer

Not all insurance companies operate in every state. Your current provider might not have a presence in your new state, or they might not offer competitive rates there. This is a perfect opportunity to shop around and get new quotes.

Update Your Vehicle Registration and Driver's License

Once you've moved, you'll need to update your vehicle registration and driver's license to reflect your new state of residence. Your insurance company will require this information.

The Future of Auto Insurance Rates What Trends to Watch

Auto insurance rates are not static; they are constantly evolving. Several trends are shaping the future of how much we pay for coverage:

Telematics and Usage-Based Insurance (UBI)

UBI programs, which monitor driving habits via devices or smartphone apps, are becoming more prevalent. Safe drivers can earn significant discounts, potentially leveling the playing field for those in historically expensive states.

Advanced Driver-Assistance Systems (ADAS)

Features like automatic emergency braking, lane-keeping assist, and blind-spot monitoring are making cars safer, which could lead to fewer accidents and lower claims. However, these systems are also expensive to repair, which could offset some of the savings.

Electric Vehicles (EVs)

The rise of EVs presents a mixed bag for insurance. They often have lower maintenance costs but can be more expensive to repair due to specialized components and battery packs. Insurers are still figuring out how to price EV coverage effectively.

Inflation and Supply Chain Issues

Economic factors like inflation, rising labor costs, and supply chain disruptions (leading to higher parts costs) are currently pushing insurance rates up across the board. This is a nationwide trend that impacts all states.

Regulatory Changes

State insurance departments constantly review and update regulations. Changes to minimum coverage requirements, how credit scores are used, or even the approval process for rate increases can all impact what you pay.

Ultimately, understanding how auto insurance rates differ across US states empowers you to make informed decisions. By knowing the factors at play, comparing providers strategically, and staying on top of your policy, you can navigate the complex world of car insurance and find the best possible rates for your location and needs.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)