How to File an Auto Insurance Claim Step by Step Guide

Follow our step by step guide on how to file an auto insurance claim. Learn the process from reporting an accident to getting your vehicle repaired.

Follow our step by step guide on how to file an auto insurance claim. Learn the process from reporting an accident to getting your vehicle repaired.

How to File an Auto Insurance Claim Step by Step Guide

Understanding the Auto Insurance Claim Process

Let's face it, nobody wants to be in a car accident. It's stressful, scary, and often leaves you wondering what to do next. But if you find yourself in this unfortunate situation, knowing how to file an auto insurance claim correctly can make a huge difference. It can save you time, money, and a whole lot of headaches. This guide will walk you through the entire process, from the moment an accident happens to getting your vehicle repaired and back on the road. We'll cover everything you need to know, including what information to gather, how to contact your insurer, and what to expect during the investigation and settlement phases. Think of this as your personal roadmap to navigating the often-confusing world of auto insurance claims.

Immediate Steps After an Auto Accident Your First Priorities

Okay, so you've just been in an accident. Your heart is probably pounding, and you might be a little shaken up. But before you do anything else, prioritize safety. This is crucial for everyone involved and for the integrity of your future claim.

Ensure Safety and Check for Injuries

First and foremost, check on yourself and any passengers. Are you okay? Is anyone injured? If there are injuries, even minor ones, call emergency services immediately. Your health and the health of others are paramount. If possible and safe to do so, move your vehicle to the side of the road or out of traffic to prevent further accidents. If your car is undrivable, turn on your hazard lights.

Contact Law Enforcement and Report the Incident

Even for minor fender benders, it's almost always a good idea to call the police. A police report provides an official, unbiased account of the accident, which can be incredibly valuable for your insurance claim. They'll document the scene, gather witness statements, and determine if any traffic laws were violated. Make sure to get the police report number and the responding officer's name and badge number. This information will be essential when you file your claim.

Exchange Information with Other Drivers and Witnesses

This is a critical step. You need to collect specific details from everyone involved. Here's a checklist of what to get:

* **Other Driver's Information:** Full name, phone number, address, driver's license number, and license plate number.

* **Insurance Information:** Their insurance company name and policy number.

* **Vehicle Information:** Make, model, year, and color of their vehicle.

* **Witness Information:** If there are any witnesses, get their names and contact information. Their perspective can be very helpful.

Remember, don't admit fault or discuss who was to blame at the scene. Stick to exchanging facts.

Document the Accident Scene Thoroughly

Technology is your friend here. Use your smartphone to take plenty of photos and videos. Capture:

* **Vehicle Damage:** Get close-ups of all damage to your car and the other vehicles involved.

* **Accident Scene:** Take wide shots showing the position of the vehicles, road conditions, traffic signs, and any relevant landmarks.

* **Skid Marks and Debris:** These can provide important clues about how the accident occurred.

* **Injuries:** If there are visible injuries, document them (with consent, if possible).

Also, jot down notes about the date, time, location, weather conditions, and a brief description of what happened. The more details you have, the better.

Notifying Your Auto Insurance Company Promptly

Once you've handled the immediate aftermath, your next step is to contact your insurance provider. Don't delay this. Most policies require you to report an accident within a certain timeframe.

Gathering Necessary Information Before Calling

Before you pick up the phone, have all the information you collected at the scene ready. This includes:

* Date, time, and location of the accident.

* Details of all vehicles involved (make, model, license plate).

* Other drivers' and witnesses' contact and insurance information.

* Police report number (if applicable).

* A clear, concise description of what happened.

* Photos and videos you took.

Having this organized will make the reporting process much smoother.

Contacting Your Insurer and Initiating the Claim

Call your insurance company's claims department. Many insurers have a dedicated 24/7 claims hotline or an online portal for reporting accidents. When you speak to a representative, be honest and factual. Provide all the information you've gathered. They will assign a claim number to your case, which you should keep handy for all future communications. They'll also likely assign a claims adjuster to your case.

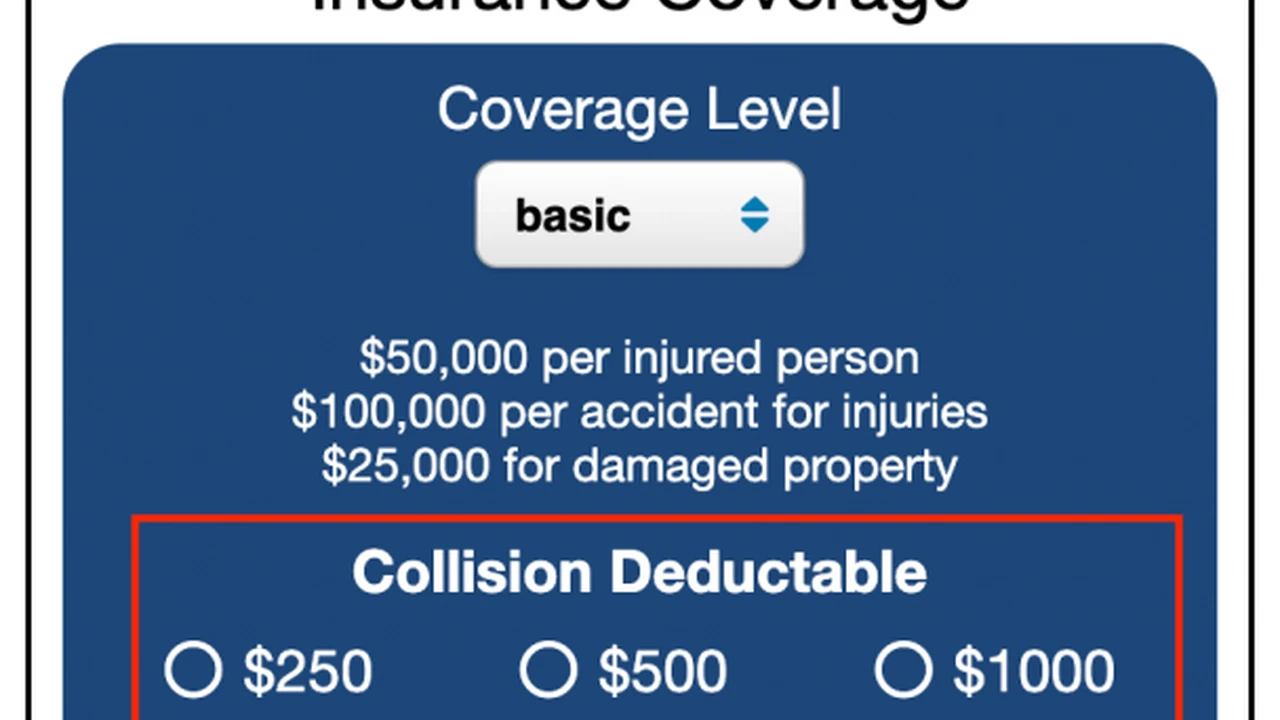

Understanding Your Policy Coverage and Deductibles

This is a good time to review your policy. Understand what types of coverage you have (e.g., collision, comprehensive, liability, personal injury protection) and what your deductibles are. Your deductible is the amount you'll have to pay out of pocket before your insurance kicks in. Knowing this upfront will help you anticipate costs.

Working with Your Claims Adjuster The Investigation Phase

After you've reported the claim, a claims adjuster will take over. Their job is to investigate the accident, determine fault, and assess the damages.

The Role of the Claims Adjuster

The adjuster will be your primary point of contact throughout the claims process. They will:

* Review the police report and your statement.

* Contact other drivers and witnesses.

* Examine vehicle damage.

* Determine fault based on the evidence.

* Estimate repair costs or total loss value.

* Negotiate a settlement.

Be cooperative and provide any additional information they request promptly.

Providing Statements and Documentation

Your adjuster will likely ask you for a detailed statement about the accident. Stick to the facts and avoid speculation. Provide all the documentation you have, including photos, videos, and any medical records if you were injured. If you have dashcam footage, that can be incredibly powerful evidence.

Vehicle Inspection and Damage Assessment

The adjuster will arrange for your vehicle to be inspected. This might happen at a repair shop, a drive-in claims center, or even at your home. They'll assess the damage and determine if your car is repairable or a total loss. If it's repairable, they'll provide an estimate for the repairs. If it's a total loss, they'll determine its actual cash value (ACV).

Repairing Your Vehicle or Settling a Total Loss Claim

Once the damage has been assessed, you'll move into the repair or settlement phase.

Choosing a Repair Shop and Getting Estimates

Your insurance company might recommend preferred repair shops, but you usually have the right to choose your own. It's a good idea to get at least two or three estimates from different reputable shops. Compare these estimates with the adjuster's assessment. If there's a significant discrepancy, discuss it with your adjuster.

Understanding Repair Process and Payment

Once you approve an estimate, the repairs will begin. Stay in communication with the repair shop about the progress. Once the repairs are complete, you'll typically pay your deductible directly to the shop, and your insurance company will pay the rest. Some insurers might pay you directly, and you then pay the shop.

Navigating a Total Loss Settlement

If your vehicle is deemed a total loss, your insurance company will offer you a settlement based on its actual cash value (ACV) just before the accident. This is not necessarily what you paid for the car, but its market value. If you have gap insurance, it can cover the difference between what you owe on your loan and the ACV. Review the settlement offer carefully. If you disagree with the ACV, you can try to negotiate by providing evidence of similar vehicles selling for a higher price in your area.

Dealing with Injury Claims and Medical Expenses

If you or your passengers sustained injuries, this adds another layer to the claims process.

Personal Injury Protection PIP and Medical Payments MedPay

Depending on your policy and state laws, your Personal Injury Protection (PIP) or Medical Payments (MedPay) coverage can help cover medical expenses, lost wages, and other related costs, regardless of who was at fault. Understand the limits of these coverages.

Working with Healthcare Providers and Submitting Bills

Seek medical attention immediately after an accident, even if you feel fine. Some injuries might not be apparent right away. Keep detailed records of all medical appointments, treatments, and expenses. Submit these bills to your insurance company promptly.

Understanding Bodily Injury Liability and Settlements

If the other driver was at fault, their bodily injury liability coverage would pay for your medical expenses, lost wages, pain and suffering, and other damages. If you were at fault, your liability coverage would pay for the other party's injuries. These settlements can be complex and often involve legal counsel, especially for serious injuries.

Common Challenges and How to Overcome Them

The claims process isn't always smooth sailing. Here are some common hurdles and how to tackle them.

Disputes Over Fault or Damage Estimates

If you and your insurer disagree on who was at fault or the extent of the damage, don't give up. Provide additional evidence, such as witness statements, dashcam footage, or independent repair estimates. You can also request a second opinion from another adjuster or invoke your policy's appraisal clause.

Delays in the Claims Process

Claims can sometimes take longer than expected. Stay proactive by regularly following up with your adjuster. Keep a log of all communications, including dates, times, and what was discussed. If delays become excessive, you can escalate the issue to a supervisor or your state's department of insurance.

Dealing with Uninsured or Underinsured Motorists

This is where Uninsured Motorist (UM) and Underinsured Motorist (UIM) coverage comes in handy. If the at-fault driver has no insurance or not enough insurance to cover your damages, your UM/UIM coverage can protect you. Make sure you have this coverage on your policy.

Specific Product Recommendations and Scenarios

While insurance policies are largely standardized, certain products and services can significantly enhance your claims experience or provide peace of mind. Let's look at a few.

Dash Cams Your Silent Witness

Dash cams are becoming increasingly popular, and for good reason. They provide irrefutable video evidence of an accident, which can be invaluable for proving fault and speeding up your claim. Imagine a scenario where another driver claims you ran a red light, but your dash cam clearly shows you had a green. Case closed!

* **Recommended Products:**

* **VIOFO A129 Pro Duo:** This is a popular choice for its excellent 4K front and 1080p rear recording quality, GPS, and parking mode. It's a bit pricier, usually around $200-$250, but offers great reliability and video clarity. Ideal for drivers who want comprehensive coverage and high-resolution evidence.

* **Garmin Dash Cam Mini 2:** A super compact and discreet option that records in 1080p. It's great if you don't want a bulky camera on your windshield. Priced around $130-$150. Perfect for those who prioritize stealth and ease of use, though it lacks a rear camera.

* **Nextbase 622GW:** A premium option with 4K recording, image stabilization, and even what3words integration for precise location reporting. It also offers an optional rear camera module. Expect to pay $300-$400. Best for tech enthusiasts who want every possible feature and top-tier video quality.

* **Usage Scenario:** Install it correctly, ensure it's always recording when you drive, and regularly check that the memory card is working. In case of an accident, immediately secure the footage.

Telematics Devices and Apps for Safer Driving

Many insurance companies now offer telematics programs (often called 'usage-based insurance' or UBI) that monitor your driving habits via a device plugged into your car's OBD-II port or a smartphone app. While primarily designed to offer discounts for safe driving, the data collected can also be useful in an accident scenario, providing objective information about speed, braking, and impact.

* **Recommended Products:** These are typically proprietary devices or apps provided by your insurance company (e.g., Progressive Snapshot, State Farm Drive Safe & Save, Allstate Drivewise). You can't buy them off the shelf.

* **Usage Scenario:** Enroll in your insurer's UBI program. Drive safely, and the data collected can not only save you money but also provide a detailed account of your driving behavior leading up to an incident, which can support your claim.

Gap Insurance Protecting Your Investment

If you finance or lease a new car, gap insurance is a smart investment. In the event of a total loss, your standard auto insurance policy will only pay out the car's actual cash value (ACV). If you owe more on your loan than the car is worth (which is common with new cars due to depreciation), gap insurance covers that 'gap' between the ACV and your outstanding loan balance.

* **Availability:** Offered by most auto insurers, car dealerships, and some banks/credit unions. Prices vary but are generally affordable, often a one-time fee or a small addition to your monthly premium.

* **Usage Scenario:** You buy a new car for $30,000, finance it, and six months later it's totaled. Your insurer pays out $25,000 (ACV), but you still owe $28,000 on your loan. Gap insurance covers the $3,000 difference, preventing you from being upside down on a car you no longer have.

Roadside Assistance Programs Beyond the Tow

While not directly related to filing a claim, having a robust roadside assistance program can significantly ease the immediate aftermath of an accident, especially if your car is undrivable. Many auto insurance policies offer this as an add-on, or you can get it through organizations like AAA.

* **Recommended Products:**

* **Your Auto Insurance Policy's Add-on:** Often the most convenient and cost-effective option, typically adding $5-$15 to your monthly premium. Services usually include towing, jump-starts, tire changes, and fuel delivery.

* **AAA Membership:** Offers comprehensive roadside assistance, often with higher towing limits and additional benefits like travel discounts. Membership tiers vary, from around $60-$120 annually.

* **Manufacturer's Roadside Assistance:** Many new cars come with a few years of complimentary roadside assistance from the manufacturer.

* **Usage Scenario:** After a minor accident, your car is drivable but has a flat tire. Your roadside assistance can send someone to change it, allowing you to get to a repair shop safely without further incident.

Final Thoughts on Navigating Auto Insurance Claims

Filing an auto insurance claim can feel overwhelming, but by understanding the process and being prepared, you can navigate it with confidence. Remember to prioritize safety, document everything, communicate clearly with your insurer, and know your rights. While we hope you never have to use this guide, having this knowledge will empower you if an accident occurs. Stay safe out there, and drive smart!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)