The Best Time to Shop for Auto Insurance Renewals

Find out the best time to shop for auto insurance renewals. Learn when to compare quotes to secure the lowest rates for your car insurance.

Find out the best time to shop for auto insurance renewals. Learn when to compare quotes to secure the lowest rates for your car insurance.

The Best Time to Shop for Auto Insurance Renewals

Let's be real, nobody loves dealing with auto insurance. It's one of those necessary evils, a recurring expense that often feels like a black hole for your hard-earned cash. But what if I told you there's a secret weapon to fight back against ever-increasing premiums? It's not a magic spell or a hidden loophole, but rather a simple strategy: knowing the best time to shop for auto insurance renewals. Timing, as they say, is everything, and in the world of car insurance, it can literally save you hundreds, if not thousands, of dollars a year.

Many drivers fall into the trap of simply letting their policy auto-renew. It's convenient, sure, but it's also a surefire way to miss out on potential savings. Insurance companies, like any business, want to retain your custom, but they also know that inertia is a powerful force. They often won't offer you their absolute best rates unless you give them a reason to – and that reason is usually the threat of taking your business elsewhere. So, let's dive deep into the optimal windows for comparing quotes and locking in those sweet, sweet savings.

Why Timing Your Auto Insurance Renewal Shopping Matters for Savings

You might be thinking, "Why does it matter when I shop? Shouldn't the rates be the same regardless?" Ah, if only it were that simple! Several factors make timing crucial when you're looking to renew your auto insurance policy. Understanding these can empower you to make smarter decisions and keep more money in your pocket.

The Power of Proactive Shopping and Early Bird Discounts

One of the biggest reasons timing is key is the concept of proactive shopping. Insurance companies love customers who plan ahead. Why? Because it signals stability and a lower risk profile. Many insurers offer what are known as 'early bird' or 'advance quote' discounts. These aren't always explicitly advertised, but they're often baked into the pricing algorithms. If you get a quote 30, 45, or even 60 days before your current policy expires, you might find significantly better rates than if you wait until the last minute. This is because insurers view last-minute shoppers as potentially desperate or less organized, which can sometimes translate to slightly higher perceived risk.

Avoiding the Auto-Renewal Trap and Rate Creep

As mentioned, auto-renewal is the enemy of savings. When your policy automatically renews, your current insurer has less incentive to offer you their most competitive rates. They know you're likely to stay put due to convenience. Over time, this can lead to 'rate creep,' where your premiums slowly but steadily increase without you even noticing, even if your driving record hasn't changed. By actively shopping around, you force your current insurer to compete for your business, and you open yourself up to better offers from competitors.

Life Changes and Policy Adjustments Opportunities

Your life isn't static, and neither should your insurance policy be. Renewals are the perfect time to reassess your coverage needs. Did you get married? Move to a new neighborhood? Buy a new car? Your old policy might not be the best fit anymore. For example, if you've paid off your car, you might consider dropping comprehensive or collision coverage to save money, especially if the car's value is low. Conversely, if you've bought a brand-new vehicle, you might want to add gap insurance. Shopping around allows you to tailor your policy to your current circumstances, ensuring you're not over-insured or under-insured.

The Golden Window When to Start Shopping for Auto Insurance Renewals

So, when exactly is this magical 'best time'? While there's no single universal date, industry experts and data suggest a prime window that gives you the best chance of securing lower rates. Let's break it down.

The 30 to 45 Day Sweet Spot Before Renewal

Most insurance professionals agree that the sweet spot for shopping for auto insurance renewals is typically 30 to 45 days before your current policy is set to expire. Some even extend this to 60 days. Here's why this window is so effective:

- Early Bird Discounts: As discussed, many insurers offer discounts for getting quotes well in advance. This is their way of rewarding proactive customers.

- Ample Time for Comparison: This window gives you enough time to gather multiple quotes, compare them thoroughly, and even negotiate with your current provider. You won't feel rushed into making a decision.

- Avoiding Last-Minute Penalties: Waiting until the last week or even the last few days can sometimes result in higher quotes. Insurers might view this as a sign of a less responsible driver, or simply that you're in a hurry and less likely to shop around aggressively.

- Opportunity for Negotiation: Having quotes from competitors in hand gives you leverage. You can call your current insurer and ask them to match or beat a competitor's offer. They'd often rather keep you as a customer than lose you entirely.

What Happens if You Shop Too Early or Too Late

While being proactive is good, there's such a thing as too early. Shopping more than 60 days out might not yield the most accurate quotes, as rates can fluctuate, and some insurers might not even be able to provide a firm quote that far in advance. On the flip side, waiting until the last week or day can be detrimental. You'll have less time to compare, potentially miss out on early bird discounts, and might end up paying more out of convenience or necessity.

Practical Steps to Take During Your Renewal Shopping Window

Now that you know when to shop, let's talk about how to do it effectively. This isn't just about getting a few quotes; it's about a strategic approach to maximize your savings.

Gathering Your Current Policy Information and Driver Details

Before you start, have all your essential information ready. This includes:

- Your current policy's declarations page (it outlines your coverage, deductibles, and premiums).

- Driver's license numbers for all drivers on the policy.

- Vehicle identification numbers (VINs) for all vehicles.

- Details of any recent accidents, tickets, or claims.

- Your current mileage and estimated annual mileage.

Having this information handy will make the quoting process much faster and more accurate.

Comparing Quotes from Multiple Insurers and Online Platforms

This is the core of the strategy. Don't just get one or two quotes. Aim for at least three to five. You can do this in several ways:

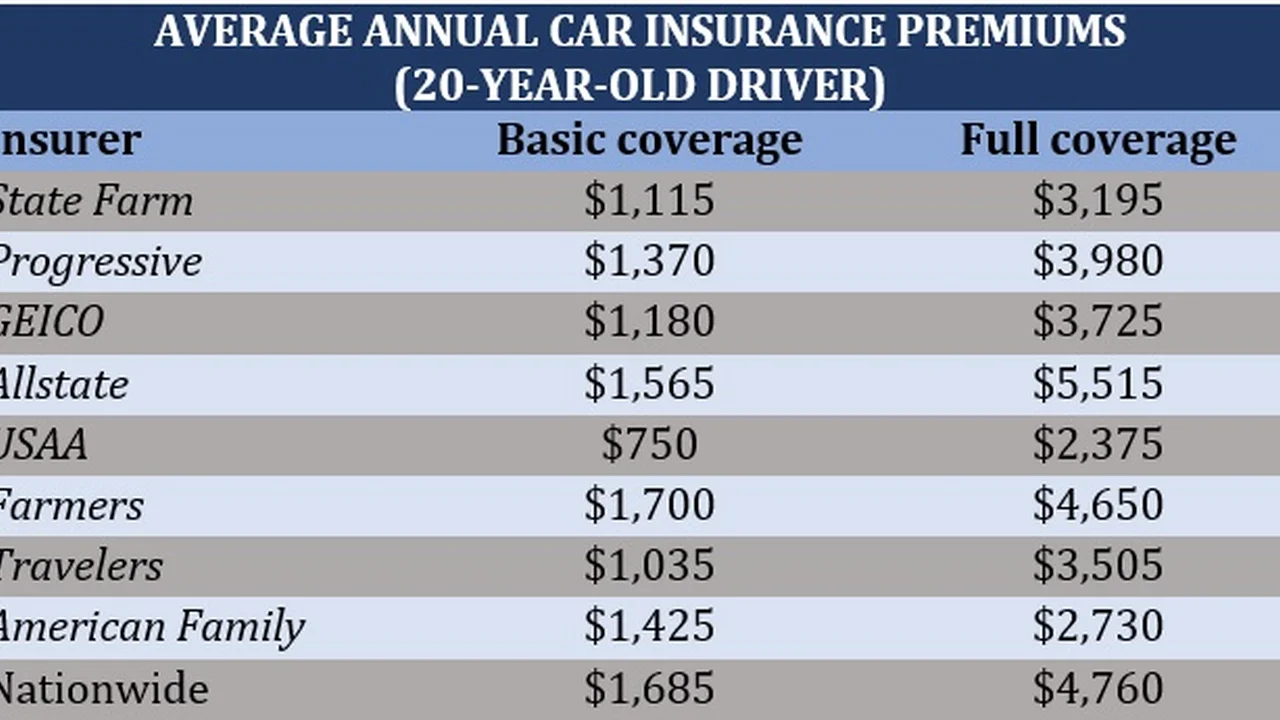

- Directly from Insurers: Visit the websites of major insurance companies like GEICO, Progressive, State Farm, Allstate, Farmers, Liberty Mutual, and smaller regional players.

- Online Comparison Tools: Websites like The Zebra, NerdWallet, or Compare.com allow you to enter your information once and get multiple quotes from various providers. These are incredibly efficient.

- Independent Agents: An independent insurance agent works with multiple carriers and can shop around for you, often finding deals you might miss. They can be particularly helpful if you have a complex driving history or unique needs.

Key Factors to Compare Beyond Just Price

While price is a huge motivator, it shouldn't be your only consideration. Make sure you're comparing apples to apples. Look at:

- Coverage Limits: Are the bodily injury and property damage liability limits the same?

- Deductibles: Are the comprehensive and collision deductibles identical? A lower premium with a much higher deductible might not be a true saving.

- Additional Coverages: Does one policy include roadside assistance, rental car reimbursement, or gap insurance that another doesn't?

- Customer Service and Claims Reputation: A cheap policy isn't worth much if the company is impossible to deal with when you need to file a claim. Check online reviews and ratings from J.D. Power or AM Best.

- Discounts Offered: Ensure you're getting all eligible discounts (multi-car, good driver, good student, defensive driving course, etc.).

Negotiating with Your Current Provider for Better Rates

Once you have competitive quotes from other insurers, don't be afraid to call your current provider. Tell them you've received lower quotes elsewhere and ask if they can match or beat them. Be polite but firm. Often, they'll be willing to adjust your premium or find additional discounts to keep your business. This is where the 30-45 day window really pays off – you have time to negotiate without feeling pressured.

Recommended Auto Insurance Providers and Comparison Tools for US and Southeast Asian Markets

To help you get started, here are some highly-rated providers and useful comparison tools, keeping in mind both the US and Southeast Asian markets. Remember, the 'best' provider is subjective and depends on your individual needs, location, and driving profile.

For the US Market

Top-Tier National Insurers (Known for broad coverage and service)

- GEICO: Often lauded for competitive rates, especially for good drivers. Their online quoting process is very streamlined.

- Progressive: Known for their 'Name Your Price' tool and Snapshot program (usage-based insurance). Good for drivers willing to share driving data for potential savings.

- State Farm: A massive insurer with a strong agent network, offering personalized service. Good for those who prefer in-person assistance.

- Allstate: Another large insurer with a wide range of coverage options and local agents. Offers various discounts like Drivewise for safe driving.

- Liberty Mutual: Provides a good balance of coverage options and discounts, including a 'RightTrack' telematics program.

Specialized or Niche US Insurers

- USAA: Exclusively for military members, veterans, and their families. Consistently ranks highest for customer satisfaction and often offers the best rates for eligible individuals.

- Amica Mutual: Known for exceptional customer service and high customer retention. Often a bit pricier but worth it for the service quality.

- Erie Insurance: Primarily serves the Midwest and East Coast. Known for strong customer service and competitive rates in its service areas.

Recommended US Comparison Tools

- The Zebra: A highly comprehensive comparison site that pulls quotes from dozens of insurers. Very user-friendly.

- NerdWallet: Offers a robust comparison tool along with in-depth reviews and financial advice.

- Compare.com: Another solid option for getting multiple quotes quickly.

For the Southeast Asian Market (Examples for Singapore, Malaysia, Thailand, Philippines, Indonesia)

The insurance landscape in Southeast Asia is more fragmented, with strong local players and international brands. It's crucial to check local regulations and specific offerings.

Singapore

- NTUC Income: A major local player, often offering competitive rates and various policy types.

- AXA Singapore: A global insurer with a strong presence, offering comprehensive coverage.

- FWD Singapore: Known for its digital-first approach and often competitive online quotes.

- DirectAsia: Specializes in direct-to-consumer insurance, often providing good value.

Malaysia

- Etiqa Takaful: A leading Takaful (Islamic insurance) provider, also offers conventional insurance.

- Allianz Malaysia: A strong international brand with a wide range of products.

- Zurich General Insurance Malaysia: Another global player with competitive offerings.

- RHB Insurance: A local bank-backed insurer with a good market presence.

Thailand

- AXA Thailand: A prominent international insurer offering various car insurance plans.

- Viriyah Insurance: One of Thailand's largest and most popular local insurers.

- Dhipaya Insurance: Another major Thai insurer with a strong reputation.

Philippines

- Pioneer Insurance: A well-established local insurer with a wide network.

- Malayan Insurance: One of the oldest and largest non-life insurance companies.

- AXA Philippines: Offers a range of insurance products, including comprehensive car insurance.

Indonesia

- ACA Asuransi Central Asia: A large and reputable local insurer.

- AXA Mandiri: A joint venture between AXA and Bank Mandiri, offering strong local presence.

- Adira Insurance: Known for its focus on motor vehicle insurance.

Recommended Southeast Asian Comparison Tools/Platforms

- GoBear (various SEA countries): While its services have evolved, GoBear was a prominent comparison platform in several SEA markets. Check local availability.

- iMoney (Malaysia, Singapore): Offers comparison services for various financial products, including insurance.

- MoneySmart (Singapore): A popular financial comparison platform.

- Local Bank Websites: Many banks in SEA offer insurance products or have partnerships, so checking their sites can be beneficial.

- Direct Insurer Websites: For the most accurate and up-to-date quotes, always visit the direct websites of the insurers operating in your specific country.

Example Scenario and Product Comparison (Hypothetical)

Let's imagine you're a 35-year-old driver in California, driving a 2020 Honda Civic, with a clean driving record. Your current policy with 'Insurer A' is up for renewal in 40 days, and they've quoted you $1,200 for the next year with 100/300/50 liability, $500 comprehensive, and $500 collision deductibles.

You decide to shop around:

- GEICO: You get an online quote for $1,050 with identical coverage. They offer a 5% 'early shopper' discount.

- Progressive: Their online quote is $1,100. They suggest trying their Snapshot program, which could potentially lower your premium by another 10-15% if you drive safely.

- State Farm (via local agent): The agent quotes you $1,250 but highlights their superior claims service and offers a multi-policy discount if you bundle your home insurance, bringing the total down to $1,180 for both car and home.

- The Zebra: You use The Zebra and find a quote from 'Insurer B' for $980, also with identical coverage, and they have good customer reviews.

Comparison and Decision:

You now have several options. Insurer B offers the lowest standalone price. GEICO is also very competitive. State Farm is slightly higher for just auto but offers bundling benefits. You call Insurer A and tell them you have a quote for $980 from Insurer B. Insurer A, wanting to keep your business, might offer to match it or come very close, perhaps at $1,000, and remind you of your loyalty discount.

In this scenario, by shopping around in the golden window, you've potentially saved $200-$220 on your auto insurance alone, or found a better overall deal by bundling. This demonstrates the power of proactive comparison.

Other Factors Influencing Your Renewal Rates and How to Manage Them

Beyond timing, several other elements play a significant role in your auto insurance premiums. Being aware of these can help you further optimize your rates.

Your Driving Record and Claims History

This is perhaps the most obvious factor. A clean driving record with no accidents or tickets will always result in lower premiums. Conversely, a history of claims or violations will drive up your rates. If you've had an incident, understand that it will likely impact your rates for 3-5 years, depending on the severity and your state's regulations. Focus on safe driving to improve this over time.

Vehicle Type and Safety Features

The car you drive significantly impacts your insurance costs. More expensive cars, sports cars, or vehicles with high theft rates typically cost more to insure. Vehicles with advanced safety features (ADAS - Advanced Driver-Assistance Systems) like automatic emergency braking, lane-keeping assist, and blind-spot monitoring can sometimes qualify for discounts, as they reduce the likelihood of accidents. When buying a new car, always get insurance quotes for different models to understand the cost implications.

Credit Score (in the US) and Financial Stability

In many US states, your credit score (or an insurance-specific credit score) is a significant factor in determining your auto insurance rates. Insurers use it as a predictor of how likely you are to file claims. A higher credit score generally leads to lower premiums. Maintaining good credit is a long-term strategy for saving on insurance. In some Southeast Asian countries, this might be less of a direct factor, but overall financial stability can still play a role in certain underwriting decisions.

Location and Demographics

Where you live and even your age and marital status can affect your rates. Urban areas with higher traffic density and crime rates typically have higher premiums than rural areas. Young, inexperienced drivers often pay the most, while rates tend to decrease in your late 20s and 30s, then potentially rise again in very old age. While you can't change your age, being aware of how location impacts rates can be useful if you're considering a move.

Mileage and Usage

The less you drive, the less risk you pose. If your annual mileage has decreased (e.g., due to working from home), inform your insurer. You might qualify for a low-mileage discount. Similarly, how you use your car (personal vs. business) affects rates. Business use typically costs more.

Final Thoughts on Mastering Your Auto Insurance Renewals

Don't let auto insurance be a set-it-and-forget-it expense. By understanding the optimal time to shop – that 30 to 45-day window before your renewal – and by actively comparing quotes, you put yourself in a powerful position to save money. Be prepared with your information, compare more than just the price, and don't hesitate to negotiate. Your wallet will thank you for the effort. Happy shopping!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)